A trading expert has outlined a possible path for Netflix (NASDAQ: NFLX) stock to climb toward $500 based on long-term technical indicators.

In a May 8 TradingView post, analyst TradingShot said the outlook is supported by Netflix’s multi-year bullish trend despite the current market correction.

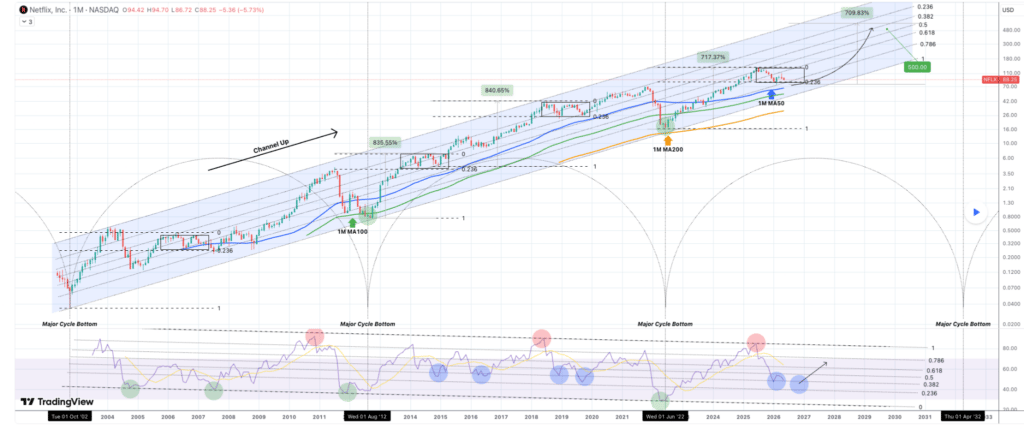

According to the analysis, Netflix has traded within a long-term rising channel since its 2002 IPO, with consolidation periods typically followed by renewed upward momentum.

After reaching an all-time high on June 30, 2025, the stock entered another correction phase, though the pattern resembles previous bullish pauses rather than the start of a prolonged bear market.

The outlook centers on the stock’s interaction with key monthly moving averages and Fibonacci retracement levels.

Historically, Netflix pullbacks during expansion cycles have retraced toward the 0.236 Fibonacci level while finding support at the monthly 50-period moving average, a pattern the current correction appears to be following.

The analysis distinguished the current setup from deeper bearish cycles that pushed Netflix toward its monthly 100-period and 200-period moving averages during major downturns, including the 2002 post-IPO collapse, the 2012 decline, and the 2022 subscriber growth crisis.

TradingShot projects that the next major bear-cycle bottom may not occur until around April 2032, suggesting the current weakness remains part of a broader bullish continuation trend.

If the monthly 50-period moving average holds, Netflix could enter a fresh expansion phase by late 2026 or early 2027, potentially mirroring the 2023–2025 rally.

Under that scenario, the stock is projected to gradually climb toward $500, with the chart placing the milestone around early October 2029, representing gains of about 480%.

Netflix stock outlook

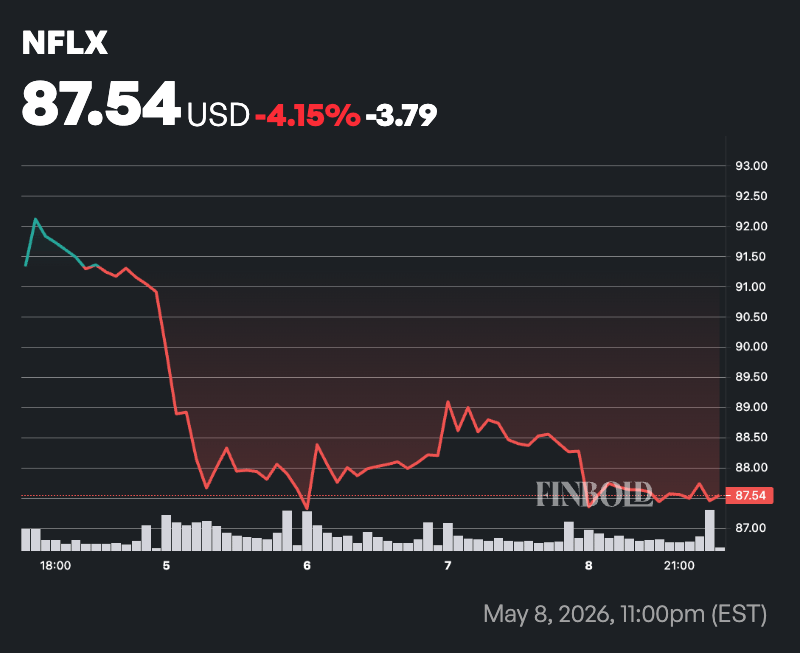

Meanwhile, Netflix shares closed at about $87 on Friday, near the lower end of their 52-week range of roughly $75 to $134, as the stock remained volatile following the company’s first-quarter 2026 earnings report despite strong fundamentals and ongoing shareholder return initiatives.

In its April 16 earnings report, Netflix posted first-quarter revenue of $12.25 billion, up 16% year-over-year, alongside earnings per share of $1.23, both above expectations.

Growth was supported by higher subscription prices, steady membership gains, and expansion in the advertising business. However, NFLX shares fell after management issued softer-than-expected second-quarter guidance and maintained its full-year revenue outlook of $50.7 billion to $51.7 billion with a projected 31.5% operating margin.

Investor sentiment improved after Netflix approved an additional $25 billion share buyback program on April 23, signaling management confidence and supporting the stock.

Advertising remains a key growth driver, with Netflix expecting ad revenue to nearly double to $3 billion in 2026 as its ad-supported tier continues attracting most new subscribers. Its advertising client base has also grown more than 70% year-over-year to over 4,000 clients.

The streaming company is also expanding deeper into live sports through the National Football League, with plans to explore more regular-season and international games to drive subscriber and advertising growth.