Following an unusually intense week of buybacks in early February and as part of a protracted program, the U.S. Treasury announced it purchased $2.5 billion of its own debt on March 4.

While the American national burden has been an ongoing and highly contentious issue, the latest government actions do not represent an effort to reduce it – indeed, with the buyback representing only 0.006% of the total debt, it hardly puts a dent in the overall figure.

Instead, it is a part of scheduled operations to improve liquidity.

Specifically, the $2.5 billion expenditure is part of a plan to repurchase $38 billion worth of bonds and part of a program that was restarted early in 2024 – under the Biden Administration – following a 22-year pause.

Elsewhere, while ensuring sufficient liquidity in the bond markets is an important factor for overall economic health, recent U.S. actions leave the question of what is being done about the national burden open.

President Trump’s efforts to reduce the national debt

While running for office, President Donald Trump pledged to help reduce expenditure and address America’s growing deficit. When elected and inaugurated, the Republican billionaire appointed, as previously promised, Elon Musk to run a new department focused precisely on eliminating ‘waste.’

At the onset, the South African-Canadian-American businessman set out to reduce expenditure by approximately $2 trillion, unleashing his Department of Government Efficiency (D.O.G.E.) – with dubious legal authority – upon the federal government to achieve the goal.

Despite these efforts and following a window of operations, President Donald Trump’s first year back in office appears, at least in terms of the deficit, lacking.

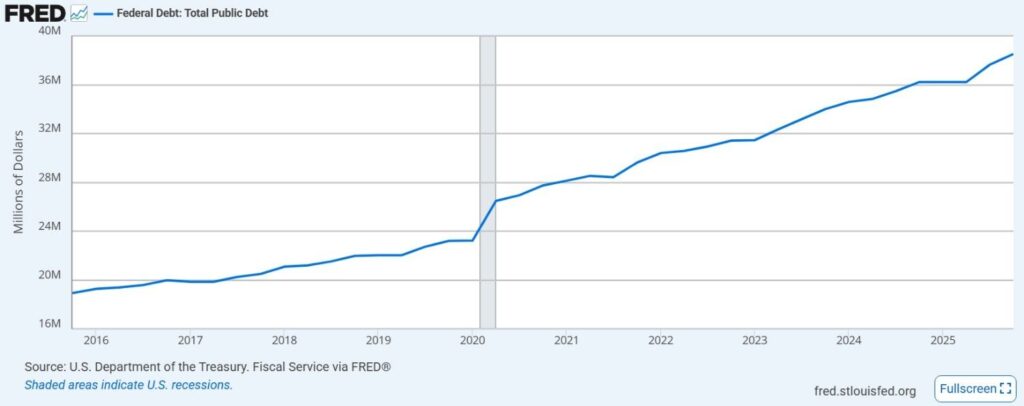

Though some media estimates placing the actual D.O.G.E. savings in the low hundreds of billions – for an approximate 90% target miss – remain unreliable, it is difficult to miss that the U.S. government debt when Trump was inaugurated stood at approximately $36.2 trillion.

Did President Trump reduce the U.S. national debt in his first year?

At press time on March 6, 2026 – some 13 months later – it is estimated at $38.8 trillion for a total increase of some $2.6 trillion. Through the entire 2024 – President Joe Biden’s final year in office – the growth of the burden came in at an estimated $2.2 trillion.

Lastly, recent political developments hint that the rate of borrowing could accelerate. Not only has the military action against Iran, which started on February 28, caused severe disruptions in the fossil fuel markets, but the Pentagon is already reportedly requesting another $50 billion to top up its weapons stockpiles.

Secretary of Defense Pete Hegseth recently stated that the U.S. has enough supplies for an indefinite campaign, and President Donald Trump – despite running on the ‘peace ticket’ and pledging the U.S. will not be involved in new ‘forever wars’ – also commented that the war would last ‘as long as it takes’ with no clear timetable.

Featured image via Shutterstock