A Bernstein analyst has reiterated a bullish call on Microsoft (NASDAQ: MSFT) stock, citing the impact of the company’s ongoing partnership with OpenAI.

In this note, analyst Mark Moerdler reiterated an ‘Outperform’ rating on the stock and maintained a price target of $641. The updated target implies roughly 50% upside from Microsoft’s press-time valuation of $424.

Moerdler’s outlook follows a recent partnership update between Microsoft and OpenAI, which he believes addresses a key overhang for investors, Microsoft’s perceived reliance on OpenAI’s models.

According to the analyst, the revised structure gives Microsoft greater flexibility to deploy a mix of internal, OpenAI, and third-party AI models depending on specific use cases. This multi-model approach reduces dependency risk while strengthening the company’s competitive positioning in the rapidly evolving AI landscape.

The investor note highlighted that Microsoft’s ability to diversify its AI stack could prove critical as competition intensifies. Over the past year, both Microsoft and OpenAI have increasingly operated with more independence, reflecting broader shifts in the AI ecosystem.

At the same time, Moerdler argued that the updated agreement should reassure investors that Microsoft can continue leveraging OpenAI’s capabilities without being locked into a single-provider strategy. Instead, decisions will be driven by performance and application-specific needs.

The partnership update comes just ahead of Microsoft’s earnings, adding a constructive backdrop to the stock. Analyst sentiment remains positive, with confidence centered on Microsoft’s adaptable AI strategy and reduced execution risk tied to external dependencies.

Wall Street bullish on MSFT stock

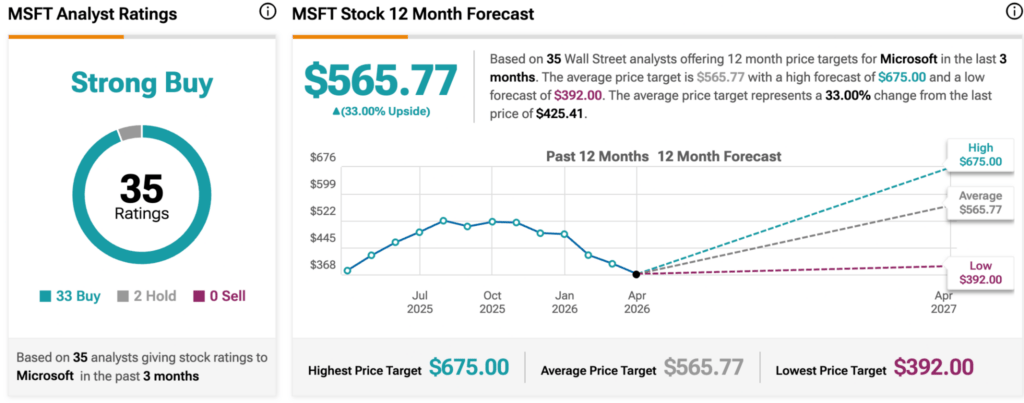

Meanwhile, broader Wall Street maintains a bullish stance on Microsoft, with the stock earning a ‘Strong Buy’ consensus rating based on 35 recent analyst reviews over at TipRanks. Of those, 33 recommend buying the stock, while two suggest holding and none advise selling, underscoring broad confidence in the tech giant’s outlook.

According to aggregated forecasts, analysts have set an average 12-month price target of $565.77, implying a potential upside of 32.63%, with a high estimate of $675 and a low forecast of $392.

Overall, analysts continue to point to the company’s strong positioning in cloud computing, artificial intelligence, and enterprise software as key drivers supporting the positive outlook.