2025 is turning out to be another challenging year for electric vehicle (EV) maker Rivian (NASDAQ: RIVN), with its stock mainly in the red due to a lack of strong catalysts to attract investors.

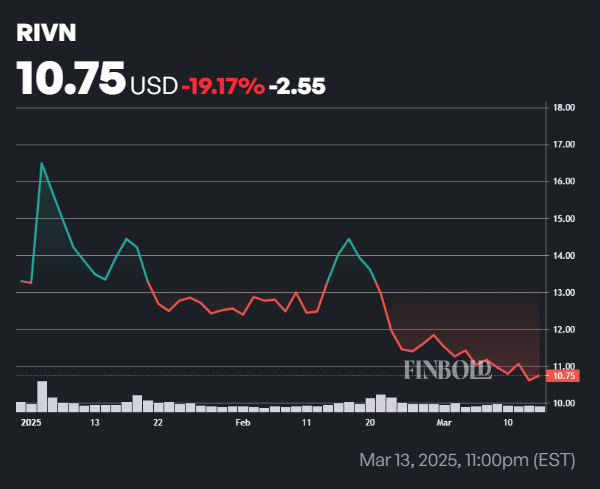

Year-to-date, Rivian shares have dropped over 18%, currently trading at $10.75. The stock gained a modest 1.3% in the last session, but the $20 resistance remains a key level for investors.

On March 16, trading expert Market Maestro observed that Rivian is hovering around critical support at $10, with technical indicators suggesting a potential breakout if macroeconomic conditions improve.

The analysis indicated that the stock remains trapped under a long-term downtrend, with a break above the descending resistance and the 23.6% Fibonacci retracement signaling a potential upside.

However, he cautioned that the Federal Reserve’s high interest rate environment and continued tightening limit growth prospects could affect the EV stock. Adding to the uncertainty, Donald Trump’s policy shifts could further disrupt Rivian’s long-term outlook.

Rivian stock fundamentals

It’s worth noting that RIVN’s struggles continue despite the company’s significant progress, especially financially. For instance, Rivian beat Q4 earnings expectations and reported its first gross quarterly profit of $170 million, a key metric.

The company aims for a “modest gross profit” in 2025 but has not projected GAAP profitability. Adjusted losses are expected to narrow to $1.7 to $1.9 billion from $2.69 billion in 2024. Rivian’s Q4 revenue was $1.73 billion, surpassing the expected $1.4 billion, while its net loss shrank to $743 million from $1.52 billion a year ago.

Meanwhile, analysts project $993.66 million in revenue for Rivian in Q1, down 17.47% year over year, but expect a 22.59% jump to $1.42 billion in Q2. Full-year 2025 revenue is forecasted at $5.39 billion, up 8.38% YoY, with 2026 surging to $7.48 billion, a growth of 38.87%.

At the same time, for long-term investors, there might be an opportunity despite the company projecting a slow 2025. Deliveries are expected to come in between 46,000 and 51,000 units, down from 51,579 in 2024. Notably, adding to potential headwinds for the EV maker is the fact that there will be no new model releases in 2025 until next year.

Some of the growth catalysts include expanding commercial sales beyond Amazon, with growing interest from businesses looking to electrify their fleets. Unique partnerships, such as Ben & Jerry’s electric ice cream trucks, point to broad potential for its delivery vans.

Additionally, Rivian’s strong product pipeline, including the upcoming R2, R3, and R3X models, is set to drive future growth. The R2, launching in 2026, will be more affordable and expand the company’s market reach, including international sales.

Wall Street sets Rivian stock price

Although Rivian’s fundamentals appear mixed, a section of Wall Street stresses that the stock has some upside potential in the coming 12 months. Specifically, 21 Wall Street analysts over at TipRanks have set an average RIVN price target at $14.34, an upside of 33.4% from the current valuation. Estimates range widely, with a high of $23 and a low of $6.10.

The analysts generally have a ‘Hold’ rating, with six recommending a ‘Buy’ and only three suggesting a ‘Sell.’

Among the analysts, on March 6, 2025, TD Cowen’s Itay Michaeli initiated coverage with a ‘Hold’ rating and a $12.70 price target on RIVN, citing a lack of near-term catalysts due to a mixed 2025 outlook and the R2 launch delay until 2026. However, he believes Rivian’s 2025 volume guidance could be conservative, and successful autonomy updates later in the year may boost investor sentiment.

Bernstein analyst Daniel Roeska is more bearish, assigning an ‘Underperform’ rating on February 27 with a $6.10 target. He expects Rivian to miss its 2024 improvement goals, citing high per-vehicle losses and slowing volume growth.

On February 25, Morgan Stanley analyst Adam Jonas stated there is an alternative upside for Rivian beyond car manufacturing, suggesting its AI-driven autonomy technology could be a key revenue driver. While acknowledging Rivian’s continued financial struggles, he highlighted its $1 billion Software & Services segment, JV with VW, and potential role in the autonomous vehicle race.

On the same date, Barclays’ Dan Levy maintained an ‘Equal Weight’ rating, raising his price target to $14. He anticipates further volatility in 2025, warning that challenges from China’s growing EV market and broader industry pressures will persist.

Featured image via Shutterstock