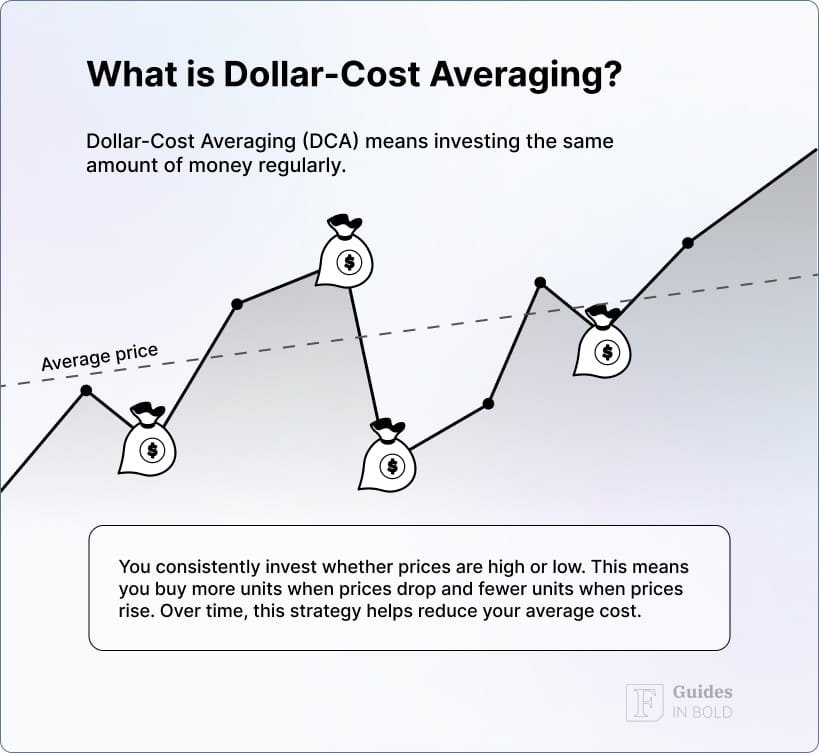

Dollar-cost averaging is a strategy whereby an investor divides up the amount to be invested across regular purchases in an effort to minimize the impact of volatility on the overall investment. Rather than aiming to time the market, they buy in at a range of different prices.

As it removes some of the dreaded mental barriers of other investment strategies, this method can be seen as a powerful behavioral tool that makes it easier for some investors to start investing.

The following guide will examine dollar-cost averaging, how and if it works, who it’s best suited for, and the pros and cons of this method.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.

Dollar-cost averaging definition

Gradually, this method tends to achieve on par or better results than aiming to buy low and sell high. But, as many experts will tell you, nobody can time the market with any consistency.

The objective of dollar-cost averaging is to lessen the overall impact of volatility on the asset price. The cost is likely to vary each time one of the regular investments is made, and thus the investment is not as highly subject to volatility. This strategy aims to keep the investor from making the mistake of making one lump-sum investment that is poorly timed.

One of the prime examples of dollar-cost averaging applications is 401(k) plans, in which regular purchases are made regardless of the cost of any given security.

Read also:

What is Value Investing?

What is Momentum Investing?

How to Buy and Sell Stocks?

Dividend Investing for Beginners

10 Best Stock Trading Books for Beginners

15 Top-Rated Investment Books of All Time

Understanding how dollar-cost averaging works

Dollar-cost averaging aims to take the emotion out of investing by having you regularly purchase the same amount of an asset. As a result, you buy fewer shares when prices are high and more when prices are low.

Let’s imagine an investor plans to invest $8,000 in ‘Mutual Fund X’ within the next eight months. They have two choices: invest all the money once at the beginning of the year, or invest $100 each month.

Though it might not appear like choosing one approach over the other would make much of a difference, if you spread out your investments in $100 monthly installments over eight months, there’s a chance you end up with more shares than you would if you bought everything at once.

How can an investor apply DCA investing strategy?

An investor can use this strategy for any investment, whether a stock, mutual fund or exchange-traded fund (ETF). But, generally speaking, dollar-cost averaging works best in bear markets and with assets that have dramatic price fluctuations. Indeed, reducing investor anxiety and fear of missing out tend to be the most important in particular at investments made in a down market.

Most commonly, DCA is used in pension accounts like 401(k) plans, in which periodic pre-determined installments are made into, typically, a mutual fund or an ETF.

Likely, the value of your investment will be moving up and down. When it goes up, you buy fewer shares, and when it goes down, you buy more shares. But in both cases, you’re spending the same amount of money—however much you’ve chosen to contribute from your paycheck.

Example of dollar-cost averaging

To better understand how dollar cost averaging works, let’s work through a hypothetical example. Say you invest $100 per month into an index fund for five months. You’ll receive a different amount of shares each time you invest $100, as share prices fluctuate at each interval. This is illustrated in the table below:

| Month | Investment ($) | Share Price ($) | Units Purchased | Total Units Held | Total Value ($) |

| 1 | 100 | 10 | 10 | 10 | 100 |

| 2 | 100 | 12 | 8.33 | 18.33 | 219.96 |

| 3 | 100 | 15 | 6.67 | 25 | 375 |

| 4 | 100 | 11 | 9.09 | 34.09 | 374.99 |

| 5 | 100 | 13 | 7.69 | 41.78 | 542.14 |

- Total investment: $500

- Average share price: $12.20

- Total units purchased: 41.78

- Final portfolio value: $542.14

- Profit: $42.14

After making equal monthly payments, your total investment at the end of five months is $500. With 135 shares at the end of the period, the investment value is $878. As a result, you would have profited $378.

It is essential to highlight the average price per share compared to what you ended up paying. In this example, the average share price at the end of the five months was $4.50 ((5+3+2+6+6.5)/5)). However, the average price you paid per share was noticeably lower at $3.70 ($500/135 shares).

Important

Does dollar-cost averaging actually work?

Beyond hypothetical examples, dollar-cost averaging doesn’t always play out neatly. Indeed, research from the Financial Planning Association and Vanguard has found that dollar-cost averaging can underperform lump-sum investing over the very long term. Thus, if an investor has access to considerable capital, they are generally better off investing it as soon as possible.

However, if you don’t have a large amount of cash saved up, waiting can cause you to miss out on potential gains. In addition, it can be nerve-wracking to invest a lot of money at once, and it may be easier mentally for you to invest parts of a large sum over a more extended period.

Nevertheless, dollar-cost averaging helps your money grow. In the former mentioned research, investors who used dollar-cost averaging did see considerable investment growth, if only slightly less most of the time than if they had invested a lump sum.

Also, it’s essential to remember that lump sum investing only beats dollar-cost averaging most of the time. A third of the time, it was DCA that outmatched lump-sum investing. Since it’s near impossible to forecast future market drops, dollar cost averaging offers substantial returns while lowering the risk you end up in the third of cases where lump-sum investing fails.

Market timing and how it compares to DCA

The opposite strategy to dollar-cost averaging is to time the market. Timing the market is an active investment strategy whereby investors buy and sell assets based on expected future price movements. It is a short-term trading strategy requiring daily, sometimes hourly, attention and close market monitoring.

While a feasible quest for experienced traders, portfolio managers, and other financial professionals, continuous perfect market timing can be tricky for the average individual investor. Not to mention that most industry experts believe it to be impossible.

Today’s low could end up relatively high next week. And this week’s high might look like a somewhat low price a month from now. But, unfortunately, it is usually only in retrospect that you can recognize any asset’s profitable prices often when it’s become too late to buy. So waiting on the sidelines and aiming to time your asset purchase, you frequently end up buying at a price that’s stagnated after it has made its juicy gains already.

On the other hand, dollar-cost averaging is a passive investment strategy. It does not require as much engagement with the market as you regularly make investments of equal sums of money. Also, rather than entering and exiting different positions, you build a position in a stock, bond, or fund.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.

Pros and Cons of dollar-cost averaging

If you’re looking to mitigate your risk and prevent emotions leading you towards incompetent investing decisions, or you fear a drop in the market, then dollar-cost averaging could be a suitable strategy. However, while this method may help mitigate some of your risks and provide more peace of mind, it might also mean you could forego some return potential.

Pros

- Dollar-cost averaging is an incredibly alluring strategy for fresh investors just starting out. It’s an excellent way to slowly but surely build wealth, even if you’re starting with a small stake;

- Dollar-cost averaging is an approach that saves investors from their psychological biases and behavioral impulses. Because traders sway between fear and greed, they are prone to get entangled in media hype or volatile market conditions, leading to poor decision-making;

- If you’re dollar-cost averaging, you’ll still be buying when other investors are selling fearfully, resulting in a lower price and setting yourself up for solid long-term gains. The market tends to go up over time, and this approach can help you acknowledge that a bear market can be a lucrative long-term opportunity rather than a threat;

- This investment strategy can also help even out share price fluctuations and potentially reduce the price you spend per share. Because you purchase more shares when prices are low, this typically means that the average cost per share you pay is lower than the average share price;

- A great technique to avoid lump-sum investing towards artificially inflated assets, which can result in purchasing a lower than desired quantity of a security;

- The strategy of adding money regularly to an investment account allows disciplined saving, as the portfolio balance increases even when its current assets are declining;

- Market timing is an art that not even market experts can master, and investing a lump sum at the wrong time can be highly costly, adversely affecting a portfolio’s value. Moreover, it is difficult to predict market swings; hence, the dollar-cost averaging strategy will flatten the purchase cost, ultimately benefiting the investor.

Cons

- Dollar-cost averaging can improve the performance of an investment over time, that only on the condition, however, that the asset increases in price. As a result, the strategy cannot protect the investor against the risk of declining market prices;

- The prevalent idea of the strategy believes that prices will, ultimately, always rise. However, employing this strategy on an individual stock without prior research on the company could prove risky. It can encourage the investor to keep buying when they should simply exit the position. Therefore, the strategy is far more secure for beginner investors on index funds rather than individual stocks;

- Systematically buying securities in small amounts over a certain period runs the risk of increasing transaction costs, potentially offsetting the gains;

- The risk-return tradeoff is simple – the potential return rises with an increase in risk. Thus, following a DCA strategy to lessen risk will inevitably lead to meager returns;

- The market typically experiences longer sustained bull markets of rising prices than the opposite. As a result, a DCA investor is more likely to lose out on asset appreciation and more significant gains than one that invests in a lump sum.

Who is dollar-cost averaging for?

Dollar-cost averaging might be right for you if you are:

- New to investing and have a limited budget;

- Want to skip time-consuming research that goes along with market timing;

- Making regular investments each month into a 401(k) retirement plan;

- Not likely to keep investing when the markets are down.

You might prefer another investment strategy if:

- You have a significant capital ready to go;

- You’re investing in mutual funds through a taxable brokerage account, that have higher initial investment minimums;

- You are comfortable with market timing and don’t mind spending additional time researching;

- You have short-term goals in mind.

How to start dollar-cost averaging?

As we’ve seen, dollar-cost averaging is a relatively simple technique and often as easy as investing in your 401(k). Indeed, you may already be dollar-cost averaging if you’re regularly contributing to a 401(k) at your workplace.

Setting up a plan with most brokerages is uncomplicated, though you’ll have to select which stock or, better yet, which well-diversified ETF you’ll purchase. In addition, you want to set up a plan to buy automatically at periodic intervals. If the brokerage doesn’t offer an automated trading plan, you can set up your own purchases on a fixed schedule, i.e., the first Friday of the month.

You can cease payments if you need to; however, the objective of DCA is to keep investing consistently, unfazed by stock prices and market anxieties. Keep in mind that bear markets, in particular, are where dollar-cost averaging shines.

What’s more, many stocks and funds pay dividends. But remember to instruct the brokerage to reinvest those dividends automatically. That makes sure you can continue to buy the stock and compound your gains over time. Of course, 401(k) reinvests your dividends as well. If it did not, you would have to pay taxes on the money and lose the tax-deferred growth.

In conclusion

To sum up, as with all investing strategies, it’s essential to consider potential returns as well as your risk tolerance.

Dollar-cost averaging is only a viable strategy if it aligns with your investing objectives. If you are investing in an asset because you believe in its long-term prospects and have decided on an amount to invest, then putting in all of your money in one lump might yield heftier gains and be the appropriate tactic for you.

However, if you want to manage your psychological urges such as greed and fear and reduce risk, or you’re afraid the market’s headed towards a drop, then dollar-cost averaging could be a sensible strategy to build your portfolio.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about dollar-cost averaging

What is dollar-cost averaging investing?

Dollar-cost averaging is an investment strategy where an investor regularly invests a certain amount of money in specific security regardless of buying price. It is the opposite of trying to time the market since you’re making instalments irrespective of market fluctuations. Instead, it aims to keep the investor from making the mistake of making one poorly timed lump-sum investment.

What are some of the advantages of dollar-cost averaging?

Dollar-cost averaging works because it removes some of the mental pressures of investing. By devoting yourself to a set schedule, you won’t have to worry about market ups and downs, making it a lot less stressful as well as less time-consuming.

What are some of the risks involved with dollar-cost averaging?

Like with any low-risk strategy, you can expect anaemic returns. Data tells us that markets do rise over time, and since DCA works best in bear markets, you might be missing out on gains you would have scored if you invested everything in one lump. Avoiding short-term volatility might mean a portion of your cash is on the sidelines and not working to build your net worth.

Who is dollar-cost averaging for?

It is excellent for beginner investors or investors trying to build more discipline with their investing practices and people with low capital as it requires little savings to get started.

What is dollar-cost averaging in stocks?

Dollar cost averaging in stocks is an investment strategy where an investor divides up the total amount to be invested across periodic purchases of equities in an effort to reduce the impact of volatility on the overall purchase. The purchases occur regardless of the asset’s price and at regular intervals.

In what ways do you, the investor saving for retirement, benefit from dollar cost averaging?

As an investor saving for retirement, you benefit from dollar cost averaging in several ways. Firstly, it helps in reducing the impact of market volatility on your investment. Secondly, it instills a disciplined approach to saving, as it encourages regular investments. Additionally, this strategy can help in avoiding the emotional decision-making often associated with timing the market, which can be particularly beneficial over the long-term horizon of retirement saving.

What is dollar-cost averaging in crypto?

Dollar-cost averaging in crypto is similar to that in stocks. It involves regularly investing a fixed amount of money into cryptocurrency, regardless of its price fluctuations.

What is reverse dollar-cost averaging?

Reverse dollar-cost averaging is an investment strategy used primarily during the withdrawal phase of an investment portfolio. Instead of investing a fixed amount regularly, as in traditional dollar-cost averaging, reverse dollar-cost averaging involves regularly withdrawing a fixed amount from an investment portfolio.

Is dollar-cost averaging a myth?

Dollar-cost averaging is not a myth; it’s a well-established investment strategy that can reduce the impact of market volatility on investment purchases, as it averages the cost of investments over time. However, there are debates about its effectiveness compared to lump-sum investing, where all available capital is invested at once. Studies have shown that lump-sum investing often outperforms DCA in terms of total returns, as markets tend to rise over time. Nevertheless, DCA can be a more emotionally and financially manageable approach for many investors.

How to calculate dollar cost averaging?

Dollar-cost averaging (DCA) can be calculated by determining a fixed investment amount and frequency (e.g., $100 monthly), recording the number of shares purchased with each investment, and then calculating the average share price by dividing the total investment by the total number of shares acquired over the chosen period, providing an average cost per share.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.