This guide will examine the man behind the largest Ponzi scheme in history– Bernie Madoff. It will investigate the ins and outs of the Bernie Madoff Ponzi scheme, how he got away with it, and the devastation he left behind as well as detail how Ponzi schemes work in general.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Related reads:

Who is Robert Kiyosaki? The Story of “Rich Dad Poor Dad”

Who is Jordan Belfort? True Story of “The Wolf of Wall Street”

Who Started Bitcoin? The True Story of Satoshi Nakamoto

Who Is Michael Burry? “The Big Short” Briefly Explained”

Who is Bernie Madoff?

Madoff kept his firm afloat by paying early investors with money raised from latecomers, a classic Ponzi scheme method. As a result, even when markets tumbled, he consistently recorded an average 11% annual gain, claiming to use an investing strategy called a split-strike conversion. In reality, however, Madoff merely deposited investor funds into a single bank account that he used to compensate existing clients who wanted to withdraw their profits.

The history’s biggest Ponzi scheme began to unravel amid the Great Recession, and as investors flocked to withdraw their money, Madoff didn’t have the funds to fulfill the stream of requests. Finally, faced with ruin, Mr. Madoff confessed to his two sons, Mark and Andrew, that his supposedly profitable money-management operation was actually “one big lie.” They reported his confession to federal authorities, and the following day, December 11, 2008, he was arrested at his Manhattan penthouse.

He was sentenced to 150 years in prison, where he died in 2021 at 82. Madoff maintained until the end that he was the sole perpetrator of his fraud and that no one, not even his family, who worked closely with him, had any idea.

Recommended video: Bernie Madoff, the greatest con in history

Bernie Madoff’s early life and education

Bernard Lawrence Madoff was born to Sylvia and Ralph Madoff on April 29, 1938, in Queens, New York. After high school, he attended the University of Alabama for one year before transferring to Hofstra University on Long Island, where he earned a bachelor’s degree in political science in 1960. Upon finishing his undergraduate studies, he briefly attended Brooklyn Law School. Ultimately, he chose to leave to pursue opportunities in the financial world, founding his own investment firm with his high-school sweetheart-turned-wife Ruth, a decision that set the stage for the trajectory of his professional life.

Bernie Madoff’s career

In 1960, using the $5,000 he earned from working as a lifeguard and sprinkler system installer (equivalent to $51,991 in 2023) and bolstered by a $50,000 loan from his father-in-law, accountant Saul Alpern (whose industry ties played a pivotal role in pushing the company forward), Madoff founded Bernard L. Madoff Investment Securities LLC, a penny stock broker-dealer. The firm operated as a sole proprietorship for 41 years but was incorporated in 2001 as a limited liability company (LLC) with Madoff as its exclusive shareholder.

At first, the company made markets (quoted bid and ask prices) via the National Quotation Bureau’s Pink Sheets. But then, to compete with companies that were members of the New York Stock Exchange trading on the stock exchange’s floor, his business began utilizing innovative computer information technology to transmit its quotes. After a trial run, the technology the firm helped design became the National Association of Securities Dealers Automated Quotations Stock Market (NASDAQ).*

Madoff Securities functioned as a third market trading provider, bypassing exchange specialist firms by directly executing orders over the counter (OTC) from retail brokers. At one point even, the firm was the largest market maker on the NASDAQ, and in 2008 as well as being the sixth-largest market maker in S&P 500 stocks indices.

Madoff is considered the first notable practitioner of payment for order flow, in which the dealer pays the broker for the right to execute a client’s order. This has been called a legal “kickback,” and the ethics of these payments have been questioned. However, Madoff argued that these payments did not alter the customer’s price and viewed them as a standard business practice.

*Madoff would become the Nasdaq chair in 1990, serving again in 1991 and 1993.

The wealth management division of Bernard L. Madoff Investment Securities LLC

Bernie Madoff’s wealth management arm was the division of Bernard L. Madoff Investment Securities LLC, where he operated his infamous Ponzi scheme, distinct from the firm’s legitimate market-making operations. The exact start of Madoff’s Ponzi scheme remains unclear. While Madoff claimed in court that the scheme began in the early 1990s, his account manager, Frank DiPascali, who joined the firm in 1975, has testified that the fraudulent activities had been ongoing “for as long as I can remember.”

Madoff’s wealth management division was shrouded in secrecy. It was marketed as an exclusive opportunity, often only available to select clients through referrals. This exclusivity, combined with consistently high returns and Madoff’s reputable standing in the financial world, made it an attractive prospect for investors.

Bernie Madoff’s sales pitch

Madoff cultivated close friendships with wealthy, influential business people, signed them as investors, paid them handsome returns, and used their positive recommendations to attract more investors. He also burnished his reputation by developing relationships with financial regulators.

As a master marketer, he exploited an air of prestige to attract serious, moneyed investors, in fact, not everyone was accepted into his funds, and it became a mark of exclusivity to be admitted as a Madoff investor. Investors who did gain access, often on word-of-mouth referral, believed they had entered the inner circle of a money-making genius.

Bernie Madoff’s alleged investment strategy

Madoff’s consistent annual returns of around 10% (typical Ponzi schemes pay returns of 20% or higher and collapse quickly) were a critical factor in perpetuating the fraud.

As mentioned earlier, Madoff claimed to use the investment strategy referred to as a split strike conversion or a collar, whereby the investor who already owns the underlying asset creates a collar by purchasing an “out of the money” (OTM) put (sell) option while simultaneously writing an OTM call (buy) option.

The put, in this case, is designed to protect the investor if the price of the stock drops. The sale of a call, on the other hand, produces income (to fund the cost of buying the put) and enables the investor to profit on the stock up to the strike (exercise) price of the call, but not higher. In short, this strategy is used to hedge against large losses, though that also limits significant upside gains.

According to Madoff, his portfolios consisted of a basket of approximately 30–35 S&P 100 stocks with a collar on the index. In 1992, he disclosed this purported method to “The Wall Street Journal”.

He insisted his returns were not that remarkable, pointing to the fact that the S&P 500 stock index generated an average annual return of 16.3% between November 1982 and November 1992, adding:

“I would be surprised if anybody thought that matching the S&P over 10 years was anything outstanding.”

In reality, though, the majority of money managers trailed the S&P 500 during that period.

Bernie Madoff’s Ponzi scheme

Madoff’s undertaking was a classic Ponzi scheme, where new investors’ money was simply funneled to fund payouts to existing investors, as well as bonuses to himself. Instead of investing the entrusted funds, investors’ money was simply deposited into an account at Chase Manhattan Bank (merged in 2000 to become JPMorgan Chase & Co.)*, where it would be retrieved to make reimbursements.

The scheme’s longevity was made possible mainly through “feeder funds,” i.e., management funds that bundled capital from other investors and poured the pooled investments into Madoff firm for management, earning millions in fees from the investors. To make matters worse, individual investors often had no idea that their money was assigned to Madoff’s care.

Bolstered by elaborate account statements and a deep reservoir of trust from his investors and regulators, Madoff was able to steer his fraud scheme safely through the dot-com crash of the early naughties and the repercussions of the 9/11 terrorist attacks. Ultimately, the economic meltdown that started in the mortgage market in mid-2007, peaking with the bankruptcy of Lehman Brothers in September 2008, was the straw that broke the camel’s back.

Somehow, Madoff kept the firm afloat even at the end of November 2008 amid a worldwide market downturn, reporting yields of 5.6%, while the same year-to-date total return on the S&P 500-stock index had been negative 38%. But the carnage was underway with hedge funds and other institutional investors, pressured by demands from their clients, withdrawing hundreds of millions of dollars from their Madoff accounts.

By December 2008, more than $12 billion had been pulled out, the feeder funds had collapsed, and little fresh capital was coming to cover redemptions. Finally, December. 10, 2008, he reportedly confessed his wrongdoing to his sons, who worked at his firm. The next day, they turned him over to the authorities. However, Bernie remained adamant that his sons were unaware of his scheme.

*The bank may have made as much as $435 million in after-tax profit from those deposits.

Bernie Madoff’s Ponzi scheme: The method

According to the SEC indictment, office workers Annette Bongiorno and Joann Crupi produced false trading reports based on the returns that Madoff had picked for each client. Specifically, once Madoff had decided on an investor’s return, the back office workers would then enter a forged trade report with an earlier date as well as a false closing trade in the exact amount required to deliver the required revenue.

Bongiorno allegedly used a computer program specially designed to backdate trades and manipulate account statements. In certain instances, returns were allegedly determined before the account was even opened.

For this scam to work, Madoff’s team on the 17th floor of the Lipstick Building, where the fraud was based, watched the daily closing price of the S&P 100. They then picked the best-performing stocks to assemble fake baskets of assets as the basis for false trading records, which Madoff insisted were achieved using his split-strike conversion approach.

Conveniently, they often made their trades at a stock’s monthly high or low, resulting in the beefy returns they flaunted to clients. Occasionally, they slipped up and dated trades as taking place on weekends and federal holidays, though somehow, this was never caught.

The aftermath of Bernie Madoff’s Ponzi scheme

Despite Madoff insisting the fraud didn’t begin until the early 1990s, according to the investigation, his scam ran for more than five decades, starting in the 1960s, costing thousands of investors their life savings.

Though the exact extent of the fraud might never be known, early investigations estimated that a whopping $65 billion of investor funds was obliterated. However, former SEC Chairman Harvey Pitt assessed the actual net fraud as between $10 and $17 billion.

The difference between the estimates derives from different calculation methods. One way calculates losses as the total amount victims thought they owed but never received. The smaller estimates are arrived at by subtracting the total money acquired from the scheme from the total money paid into the scheme after excluding collaborators, those who invested through feeder funds, and those who received more cash from the scheme than they put in.

Almost half of Madoff’s investors were net winners, earning more than their investments. However, profit withdrawals in the final six years were subject to clawback (return of money) lawsuits.

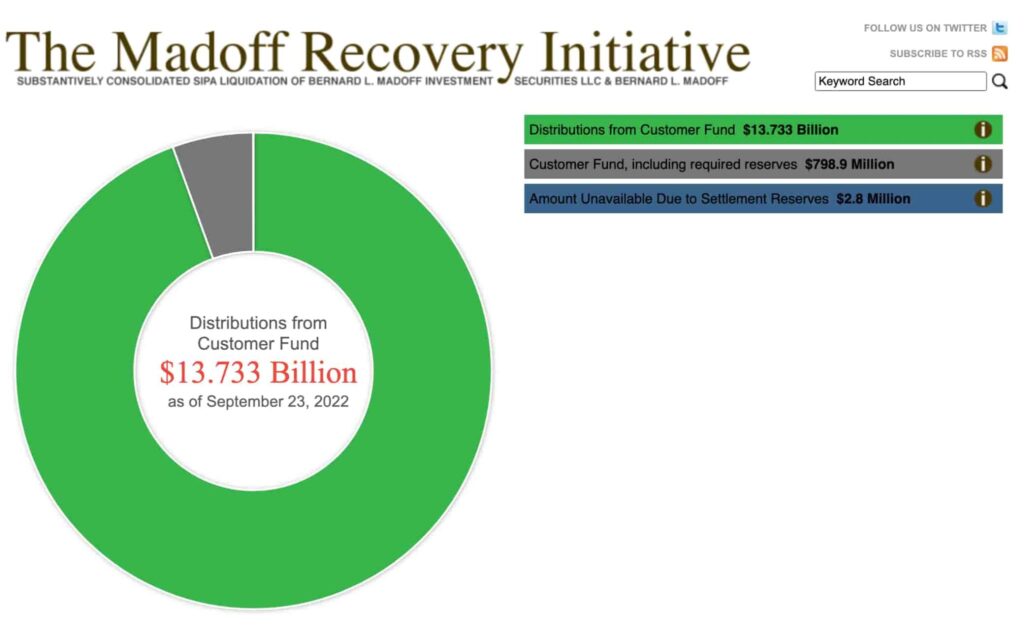

The Madoff Recovery Initiative sued those who profited from the Ponzi scheme, and as of October 2022, almost $14 billion in total recoveries and settlement agreements have been reported. In addition, the Madoff Victim Fund (MVF) was created in 2013 by the Department of Justice to help compensate those Madoff defrauded. As a result, approximately $4 billion has been distributed to 40,454 Madoff victims in the U.S. and worldwide, recovering 88.35% of victims.

Even more devastatingly, investors lost more than money. At least two people, in despair over their losses, died by suicide. Additionally, a prominent Madoff investor suffered a fatal heart attack after months of litigation over his role in the fraud. Even Madoff couldn’t escape the dire aftershocks of his own doing. His older son, Mark, died by suicide on December 11, 2010, exactly a year after his father’s arrest.

Bernie Madoff in films and television

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

What is a Ponzi scheme?

Because no real profits are being made, Ponzi schemes must try and avoid too many investors withdrawing their earnings. They do this by encouraging them to stay in the game, i.e., reinvest the money and earn even more. High returns often incentivize clients to leave their money in the scheme so that the operator doesn’t have to pay much back to them.

Instead, the operator sends account statements boasting high profits, maintaining the deception of an investment with high returns. Ultimately, all they need to do is tell investors how much they are making periodically without actually providing any tangible returns.

In addition, operators also try to minimize withdrawals by offering new plans to investors where funds cannot be withdrawn for a certain period in exchange for higher returns. As a result, the scheme sees new cash flows as investors cannot get their money out of the investment.

However, suppose a few investors wish to withdraw their money per the agreed-upon terms. In that case, their requests are usually promptly processed, giving all other investors the illusion that the fund is solvent and financially sound.

Ponzi schemes use vague verbal guises such as “hedge futures trading,” “high-yield investment programs,” or “offshore investment” to describe their trading strategy. In addition, it is common for the schemers to exploit the lack of investor knowledge and claim to use proprietary, secret investment methods to avoid sharing information about the scheme.

Without legitimate income, Ponzi schemes need a constant flow of new investments to continue to provide returns to earlier backers. So, when it becomes hard to recruit new investors or large numbers of existing investors cash out, these schemes collapse, resulting in most investors losing all or much of the money they invested.

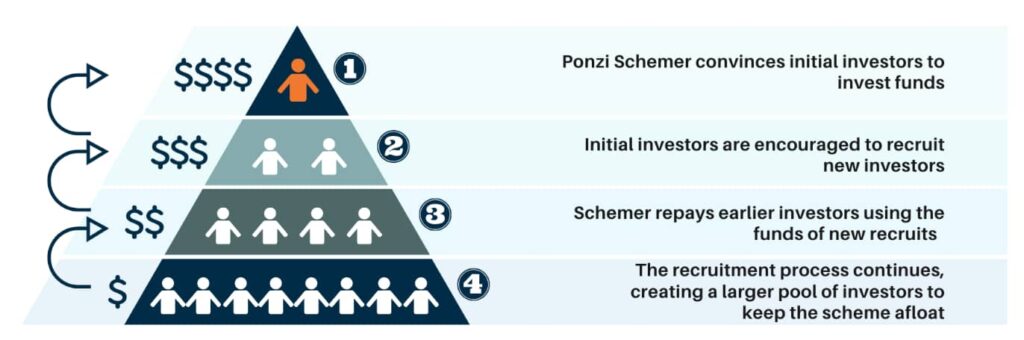

How does a Ponzi scheme work

Let’s imagine a basic example where Anna promises a 10% return on investment to her friend Kate. Kate gives Anna $1,000 with the expectation that the value of the investment will be $1,100 in one year. Next, Anna promises 10% returns to her friend Paula. Paula then agrees to give Anna $2,000.

With $3,000 now in hand, Anna can deliver on her promise to Kate by paying her $1,100. Additionally, Anna can steal $1,000 from the collective pool of funds if she believes she can get further investors to give her money. In short, Anna must continually get cash from new clients to pay back older ones for this plan to work.

Recommended video: I ran a nightclub Ponzi scheme at 19

History of the Ponzi scheme

The term “Ponzi scheme” was coined in 1920 after the con artist Charles Ponzi.

However, some of the first recorded incidents to meet the modern definition of this sort of investment fraud were carried out in the mid-to-late 1800s by Adele Spitzeder in Germany and by Sarah Howe in the United States. For example, through the “Ladies’ Deposit,” whereby Howe offered an entirely female clientele an 8% monthly interest rate and then just ran with the money that had been invested.

Furthermore, the methods of what came to be known as the Ponzi were also previously described in two of Charles Dickens’s novels: “Martin Chuzzlewit” (1844) and “Little Dorrit” (1857).

Charles Ponzi’s original scheme in 1919 was based on a legitimate form of arbitrage by which he would buy discounted postal reply coupons in other countries and redeem them at face value in the U.S. Under his company, Securities Exchange Company, he promised clients returns of 50% in 45 days or 100% in 90 days.

In reality, however, Ponzi was paying earlier investors using the investments of later investors. The scheme operated for over a year before it collapsed, costing his investors $20 million.

Ponzi’s gained considerable press coverage within the United States and internationally, both while it was being perpetrated as well as after its demise. Eventually, this notoriety led to this type of scheme being named after him.

Signs of a Ponzi scheme

According to the Securities and Exchange Commission (SEC), most Ponzi schemes share the following characteristics:

- A promise of high returns with little or no risk;

- Excessively consistent returns regardless of overall market conditions;

- Investments that are not enlisted with the SEC or with state regulators;

- Unlicensed or unregistered sellers;

- Secret investment strategies that are too complex to explain;

- Errors with paperwork;

- Difficulty withdrawing funds.

Crypto Ponzi scheme

Ponzi schemes are notorious for enticing impressionable investors by leveraging their esoteric strategies or superior knowledge of a “new technology” as a selling point. And unfortunately, the con artists running them often have extraordinary sales skills that enable them to exploit the hype behind cryptocurrency booms, promising sky-high returns as they lean on our inherent fear of missing out on a good deal.

Crypto has been a prime target for the new generation of Ponzi scheme masterminds since 2016, when the market gained mainstream prominence. Indeed, crypto market and products are the perfect playing ground for schemers because average investors don’t fully grasp the technology behind crypto nor know how to assess it as a solid investment. Crypto itself has also been described as a Ponzi scheme, including by an Oxford University scholar and the CEO of JP Morgan.

Additionally, unlike traditional investments where investors can inspect the company’s earnings, third-party research reports (i.e., Morningstar), or regulatory documents, many crypto products are unregulated, with little information to be found.

Ponzi schemes have also become rife in the sector due to the decentralized nature of blockchain technology, enabling scammers to evade regulatory authorities who would otherwise flag or freeze suspicious transactions. Furthermore, the immutable nature of blockchain technology that makes it impossible for any entity (e.g., a government) to manipulate data stored on the network also works in the schemers’ favor by making it harder for victims to get their money back.

For example, let’s consider the GainBitcoin scam that duped its victims of more than $12.8 billion, possibly the largest crypto Ponzi sham to date. It promised its clients yields of 10% in Bitcoin-on-Bitcoin deposits, where investors were enticed to lend the company Bitcoins (BTC) on the promise that their investments would be increased by the set 18-month period. Unfortunately, since the number of Bitcoins is limited, the model was not viable.

How to avoid Ponzi schemes?

Though most people would jump at the opportunity to put their money into a fail-safe investment that promises above-market returns, we know that if it sounds too good to be true, it probably is. So to make sure you don’t become a victim of a Ponzi scheme, one that has ripped off unsuspecting investors for tens of billions of dollars, abide by the techniques below:

- Stay skeptical: Be wary of investments that boast unusually high or immediate returns with little or no risk. If you sense that the investment is particularly exotic or unfamiliar, you may want to avoid putting money in it;

- Beware of unsolicited offers: Someone contacting you unexpectedly with a “chance of a lifetime” or a “get rich fast” slogan is often a huge warning sign;

- Do the research: Research the broker, brokerage firm, or financial advisor using the Financial Industry Regulatory Authority’s (FINRA) BrokerCheck. Verify that the operator is licensed and scan for any negative information;

- Verify the investment’s credentials: Find out if the investment is registered with the proper regulator, such as the SEC or state regulator, or is exempt from registration (and if so, why);

- Understand the investment: Avoid putting money into an investment you don’t fully understand. In particular, avoid investments that use proprietary, or too-complex-for-laymen trading methods, which are often just a gimmick to avoid questioning. Many online resources help you learn how to invest and evaluate opportunities for risk and potential gain, including here at Finbold.

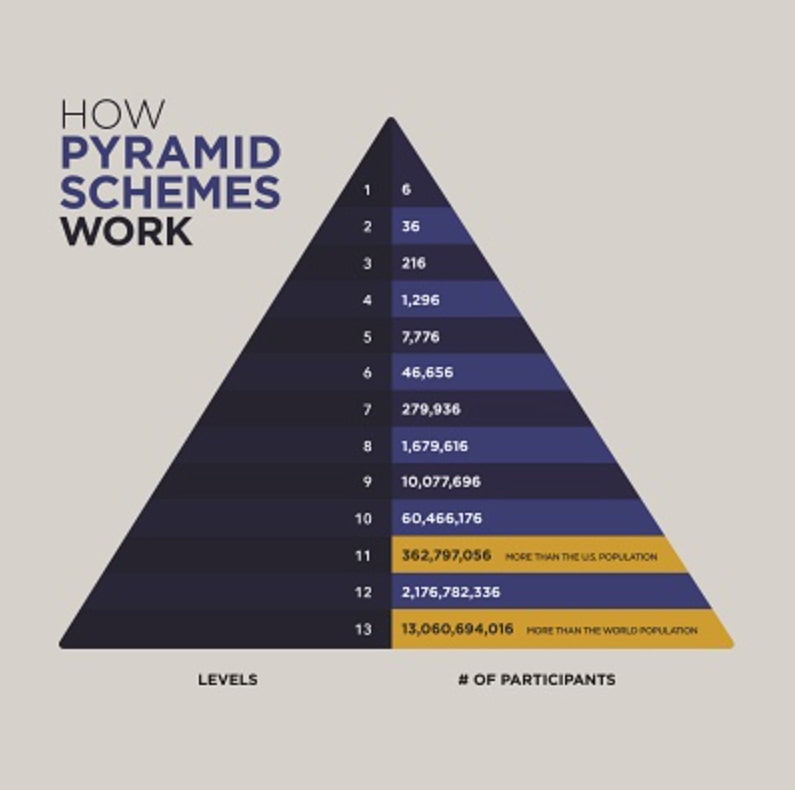

What is a pyramid scheme?

Now that we’ve clarified what a Ponzi scheme is (using income from other new investors to pay off older ones), let’s look at what a pyramid scheme is. A pyramid scheme is a fraudulent business model that earns money by recruiting new members or sellers but claiming they earn money via product sales.

The basis of the scheme is that money from newer recruits will pay off the earlier participants and that later recruits won’t have a chance (or lower chances) to earn money with the scheme. Bernie Madoff’s pyramid scheme, or Ponzi scheme, is one of the most notorious pyramid schemes, as it follows the same principle.

Pyramid scheme vs Ponzi scheme

Both Ponzi and pyramid schemes lure in unsuspecting investors with promises of extraordinarily high rates of return. But because they are based on using new investors’ funds to pay the earlier investors, both schemes eventually collapse when the pool of available and new participants dries up, and there isn’t enough money to go around.

Recommended video: Pyramid Schemes and Ponzi Schemes Explained in One Minute

While both are devastating, there are, however, significant differences between the two ploys:

- Structure: With Ponzi schemes, investors give money to a portfolio manager, who is in charge of redistributing any profits with the incoming funds contributed by later investors. With pyramid schemes, the initial schemer recruits other participants, who recruit additional participants, and so on. The scheme then funnels earnings from all recruited participants on lower levels of an organization to participants on higher levels. Pyramid schemes rely on income from recruitment fees and not, as victims may believe, from the sale of goods;

- Product: Ponzi schemes are based on fraudulent investment management entities that promise a high return. Pyramid schemes present an investment opportunity, such as the right to sell a particular product or service;

- Promise: A Ponzi scheme claims to rely on some obscure investment method with promised returns on a later date. In contrast, pyramid schemes often explicitly claim that new capital (i.e., new investors) will be the source of payout for the initial investments, above all encouraging recruitment of new members;

- Lifespan: Pyramid schemes generally collapse much faster since they demand exponential growth in participants to sustain them. Ponzi schemes, on the other hand, can survive merely by persuading most existing participants to reinvest their earnings with a small number of new players.

In conclusion

Madoff’s Ponzi scheme became a symbol of corporate greed and unapologetic dishonesty on Wall Street, that, in the eyes of many, led to the financial meltdown of 2008. Yet, while Madoff was sentenced to 150 years with $170 billion in restitution, no other prominent Wall Street figure faced legal ramifications in the wake of the crisis.

And though the warning signs pointing to fraud were there, investors, as well as federal regulators, seemed to (willfully) ignore them. So ultimately, it came down to greed and the innate fear of missing out, as well as Madoff’s marketing genius and status in financial circles to overrule the red flags.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about Bernie Madoff and Ponzi schemes

Who is Bernie Madoff?

What else is Bernie Madoff known for?

Madoff’s firm helped develop the technology that became the National Association of Securities Dealers Automated Quotations Stock Market (NASDAQ). Additionally, he is considered the first prominent practitioner of payment for order flow, in which the dealer pays the broker for the right to execute a client’s order, though the ethics of these payments have been questioned.

What did Bernie Madoff do?

Bernie Madoff was behind the history’s biggest Ponzi scheme. Madoff claimed to use the investment method referred to as a split strike conversion, whereby the investor who owns the underlying asset hedges against volatility by purchasing options contracts on that same asset.

What is a Ponzi scheme?

A Ponzi scheme is a fraudulent investment ploy that pays existing investors with money collected from new investors rather than legitimate investment earnings. Fraudsters behind these schemes often promise high returns with little or no risk. A Ponzi scheme remains sustainable as long as there is a constant influx of new investors and as long as most investors do not demand full reimbursement and keep reinvesting their profits.

What's the difference between Ponzi and pyramid scheme?

The primary difference between a Ponzi scheme vs. Pyramid scheme two cons is the structure. While pyramid schemes work top-down, involving multiple levels of participants, Ponzi schemes have a more circular design centered around the fraud operator, with all investors on equal, illegitimate footing. The significant similarity between the two is that both require a continual stream of investors to sustain themselves.

How did Bernie Madoff die?

Bernie Maddoff died of natural causes (hypertension, atherosclerotic cardiovascular disease, and chronic kidney disease) at the age of 82 in 2021 in Federal Medical Center, Butner, while serving a 150-year sentence in prison after being arrested on December 11, 2008.

What was Bernie Madoff's net worth at death?

Celebrity Net Worth puts Madoff’s net worth at death at -$17 billion. Bernie Madoff’s net worth at peak was estimated to be between $823 million and $826 million.

What is Ruth Madoff's net worth?

According to Celebrity Net Worth, Ruth Maddoff’s net worth is $2 million.

What did Madoff do with the money?

Madoff used the money from new investors to pay returns to earlier investors, which is the hallmark of a Ponzi scheme. While some funds were used to maintain his lavish lifestyle and that of his family, the majority created an illusion of genuine and consistent returns to attract more investors.

How did Madoff get caught?

Madoff’s scheme began to unravel during the financial crisis of 2008 when he couldn’t meet withdrawal requests from his clients. Finally, December. 10, 2008, he reportedly confessed the insolvency of his operations to his sons, Mark and Andrew. Shocked by the revelation, they reported their father to federal authorities, leading to his arrest and subsequent prosecution for orchestrating the largest Ponzi scheme in history.

Were Bernie Madoff's sons involved in his scheme?

Bernie Madoff’s sons, Mark and Andrew, worked at his firm but maintained their innocence and were never prosecuted for involvement in the scheme.

Why did Madoff do it?

Madoff’s motives are multifaceted. He seemed to be driven by a desire to maintain his reputation, ensure consistent returns for his clients, and uphold the illusion of success. Over time, the scheme grew, and the pressure to deliver results might have made it increasingly challenging to stop without revealing the deceit.

What happened to Bernie Madoff's family?

The Bernie Madoff family faced significant scrutiny and hardship following the exposure of the Ponzi scheme. Madoff’s wife, Ruth, was ostracized by many and had her assets significantly reduced. Their sons, Mark and Andrew, faced legal inquiries, public disdain, and personal challenges. Tragically, Mark took his own life in 2010, and Andrew died of lymphoma in 2014.

Are there any books about Bernie Madoff?

Some of the best books about Bernie Madoff and his Ponzi scheme include “The Wizard of Lies: Bernie Madoff and the Death of Trust” by Diana B. Henriques, which offers an in-depth look at Madoff’s scheme and its impact; “No One Would Listen: A True Financial Thriller” by Harry Markopolos, the whistleblower’s account of trying to expose Madoff; and “Betrayal: The Life and Lies of Bernie Madoff” by Andrew Kirtzman, a detailed biography that traces Madoff’s rise and fall. These books provide comprehensive insights into Madoff’s fraudulent activities and their consequences.

What podcasts cover the story of Bernie Madoff?

Several podcasts delve into Bernie Madoff’s story. Ponzi Supernova presents a detailed portrait of Madoff and his scheme’s mechanics. The episode “Madoff Behind Bars” of American Greed Podcast focuses on Madoff’s thoughts and prison life, providing insights into his fraudulent activities. Additionally, the Swindled Podcast covers various true crime stories, including episodes dedicated to Madoff’s Ponzi scheme, offering a broader context of financial fraud and deception.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.