In this guide, we will examine the Great Recession, how it came about, its effects on the United States economy, the eventual path to recovery as well as the legacy it left behind.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Summary

– Definition: Severe global downturn from 2007–2009; worst since the Great Depression;

– Cause: Burst of the U.S. housing bubble and collapse of mortgage-backed securities (MBS);

– Root issues: Deregulation, subprime lending, risky derivatives (CDOs, CDS), inflated credit ratings;

– Impact: GDP fell 4.3%, unemployment peaked at 10%, 8.8M jobs lost, $19T in wealth erased;

– Bank failures: Bear Stearns, Lehman Brothers; massive credit crunch and Wall Street crash;

– Govt. response: TARP ($700B bank bailout), ARRA stimulus, near-zero interest rates, QE;

– Long-term effects: Slow recovery, especially for Millennials; tighter regulations via Dodd-Frank;

– Lesson: Excessive risk-taking and lack of oversight can destabilize global economies.

The Great Recession definition

The recession was primarily caused by deregulation in the financial industry, which allowed banks to engage in hedge fund trading with sophisticated derivative products such as mortgage-backed securities (MBS)—in turn, creating more demand for mortgages to maintain the profitable sale of these derivatives. As a result, interest-only loans began being marketed to subprime lenders with bad credit.

In 2004, the Federal Reserve raised the Fed funds rate just as the interest rates on these new mortgages reset. As supply outpaced demand, housing prices plummeted in 2007, trapping homeowners who couldn’t afford their loans in the first place. As borrowers began to default on their mortgages, the value of mortgage-backed securities held by investment banks crumbled, causing several to collapse or be bailed out by the government.

The combination of banks unable to lend to businesses and homeowners paying down debt rather than borrowing and spending resulted in the Great Recession that began in the U.S. officially in December 2007, extending over 18 months.

From the start of the crisis in December 2007 to its official end in June 2009, real gross domestic product (GDP) dropped by 4.3%, and unemployment increased from 5% to 9.5%, peaking at 10% in October 2009.

Recommended video: Warren Buffett Explains the 2008 Financial Crisis

Beginners’ corner:

- What is Investing? Putting Money to Work

- 17 Common Investing Mistakes to Avoid

- 15 Top-Rated Investment Books of All Time

- How to Buy Stocks? Complete Beginner’s Guide

- 10 Best Stock Trading Books for Beginners

- 15 Highest-Rated Crypto Books for Beginners

- 6 Basic Rules of Investing

- Dividend Investing for Beginners

- Top 6 Real Estate Investing Books for Beginners

- 5 Passive Income Investment Ideas

What caused the Great Recession?

The chief culprit in the Great Recession was the implosion of mortgage-backed securities and the subsequent housing market collapse. However, many other factors contributed to the crisis, including lax lending standards, government housing policies, and poor regulation in the banking industry. Let’s examine these aspects and more in greater detail.

Deregulation and repeal of the Glass-Steagall Act

The two decades preceding the Great Recession were predominantly prosperous, with rises in GDP, low inflation, and two relatively mild recessions.

The period from the mid-1980s to 2007 was dubbed the Great Moderation and is characterized by the reduction of observed business cycle (a process of continuous economic expansion and contraction) volatility, which had been overcome in favor of modest but steady economic growth.

However, excessive optimism led to lavish spending, particularly for risk-tolerant investors. Indeed, everyone from homeowners to bankers believed the economy would keep growing, making traditionally risky behavior seem safe.

Assumptions about endless economic growth also contributed to a period of deregulation, most significantly the 1999 repeal of the Glass-Steagall Act, Depression-era legislation that separated commercial and investment banking activities. This was done by establishing the Gramm-Leach-Bliley Act, or the Financial Services Modernization Act, which eliminated the Glass-Steagall Act’s restrictions.

The rollback of the Glass-Steagall Act allowed banks and brokerages to expand and opened the floodgates for giant mergers, creating entities that were too big to fail, i.e., the economy could not take the hit of their failure– precisely the reason they later had to be bailed out by the U.S. government. In addition, it spurred commercial banks into taking on risky and speculative investments to boost their profits.

Low-interest rates and lax lending standards

Confronted with the dot-com bubble’s collapse and 9/11, the Federal Reserve lowered the Feds fund rate from 6.5% in May 2000 to 1% in June 2003, resulting in rapid economic growth and increased demand for homes and mortgages. To fully exploit the boom, mortgage lenders rushed to approve as many home loans as possible, including for borrowers with poor or no credit history, by offering subprime loans.

Because these loans were granted to individuals who previously hadn’t qualified for conventional mortgages, it opened the market to a torrent of new homebuyers, resulting in greater demand for homes. Ultimately, this contributed to the vast increase in housing prices, leading to the rapid formation (and eventual bust) of the 2000s housing bubble.

Many subprime mortgages were adjustable-rate mortgages (ARM), where interest rates rise along with the Fed funds rate. As a result, borrowers already on shaky financial footing stood little chance of being able to make payments when the interest rate increased in the following years.

Unfortunately, in a rush to take advantage of a hot market and low-interest rates, many homebuyers took on loans without fully understanding the terms. But, in reality, these subprime loans were only safe until housing prices rose and interest rates stayed down.

Increase of unregulated derivative products

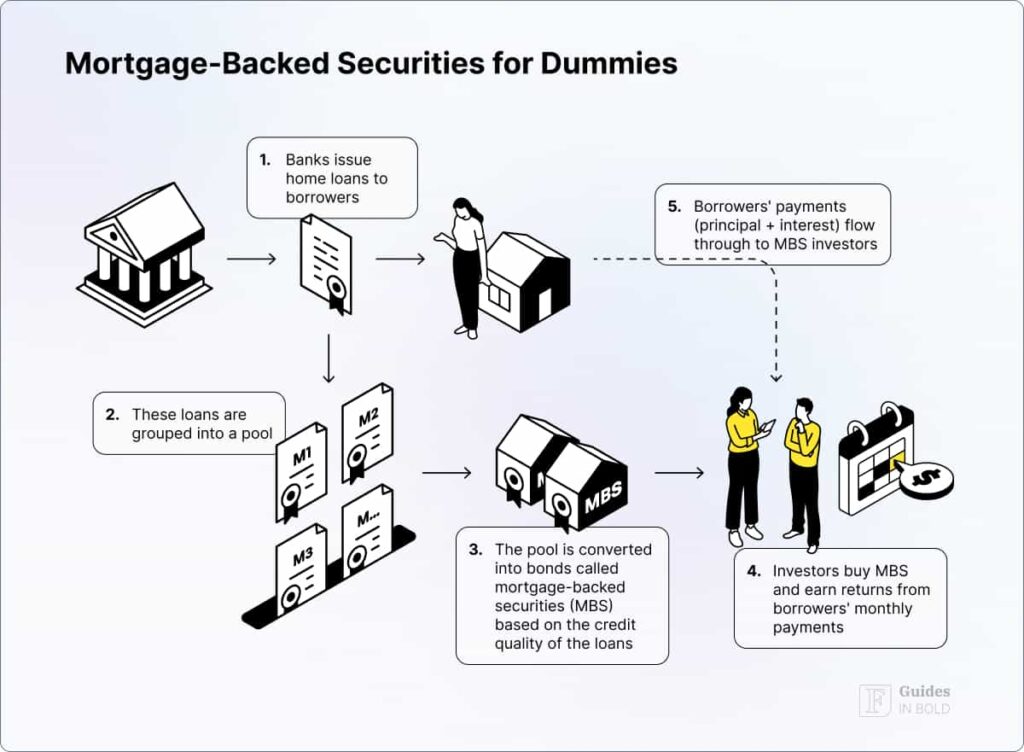

To fund these risky subprime mortgages and to free up capital, banks would sell their mortgages to the country’s two biggest home lenders, Fannie Mae and Ginnie Mae, who then resold them in a bundle with other mortgages (creating an MBS) on the secondary market.

Eventually, an investment bank or hedge fund divided these mortgage-backed securities into similar risk profiles known as tranches and marketed them to investors.

The profitability of MBS generated more demand for the mortgages they were backed by, further encouraging banks to write loans to unqualified borrowers to keep the supply of derivatives flowing. In addition, Freddie Mac and Fannie Mae aggressively backed the market by issuing scores of MBS. But unfortunately, the MBS created were increasingly low-quality, high-risk investments.

Furthermore, the underlying loans of these derivative products were often rated incorrectly, inflating their value and misleading investors. Moreover, they could be made up of a pool of prime loans, near-prime loans (called Alt.-A loans), risky subprime loans, or a combination of the above, making them impossible to price.

Mortgage-backed securities were typically held by hedge funds and other financial institutions, but they were also in pension funds, corporate assets, and mutual funds. And since the financial markets seemed stable overall, investors felt secure about taking on more debt.

Ultimately, banks had sold more MBSs than what could possibly be supported by solid mortgages. But they seemed secure because they also bought credit default swaps (CDS), another financial derivative, to insure against the risk of defaults.

Banks and hedge funds started trading swaps on MBSs and CDOs in unregulated transactions. Furthermore, because CDS transactions didn’t show up on institutions’ balance sheets, investors couldn’t evaluate the actual risks these enterprises had assumed.

But when the MBS market caved in, insurers did not have the capital to cover the CDS holders. Insurance giant American International Group (AIG) sold these swaps, and when the MBSs eventually lost value, they didn’t have enough capital to fulfill all the swaps.

In 2007, as the value of these derivatives plummeted, banks began to panic and cut back on lending, causing a credit crunch (a reduction in lending activity by financial institutions brought on by a sudden shortage of capital). They didn’t want other banks to give them worthless mortgages as collateral, so interbank borrowing costs (Libor), increased. The Fed began pumping liquidity into depository institutions via the Term Auction Facility (TAF), but that wasn’t enough.

In the end, the unprecedented spread of these complex financial products, including MBS, CDOs, and CDSs, created a domino-like housing market collapse, the main reason why the financial crisis was so widespread.

Reckless rating standards

Because a large section of the debt securities market was restricted in their bylaws to holding only the safest securities, i.e., securities the rating agencies designated AAA, MBS, and CDOs could not have been marketed without ratings by the Big Three rating agencies: Moody’s Investors Service, Standard & Poor’s Global Ratings, and Fitch Ratings.

Part of the problem was that despite the risk, the agencies continued to give the derivatives products ratings that were too positive, leading many investors to believe that these investments were safe.

Critics have claimed there was an inherent conflict of interest for agencies: between accommodating investment banks (who also threatened to withdraw their business if they didn’t receive the desired rating) for whom higher ratings meant higher earnings and accurately rating the debt for the benefit of the debt buyer/investor, who provide no revenue to the agencies.

The Financial Crisis Inquiry Report (FCIR) concluded that the “failures” of rating agencies were “essential cogs in the wheel of financial destruction” and “key enablers of the financial meltdown.” It went on to say:

“The mortgage-related securities at the heart of the crisis could not have been marketed and sold without their seal of approval. Investors relied on them, often blindly. In some cases, they were obligated to use them, or regulatory capital standards were hinged on them. This crisis could not have happened without the rating agencies. Their ratings helped the market soar, and their downgrades through 2007 and 2008 wreaked havoc across markets and firms.”

The housing bubble bursts

After staying low throughout the early 2000s, the Fed began to raise interest rates from 2004 through 2006 to maintain stable inflation rates. In mid-2004, the Fed funds rate was 1.25%, but by mid-2006, it had risen to 5.25%, remaining as such until August 2007.

New credit flows into real estate moderated in response to rising interest rates. But, even more seriously, the existing adjustable rate mortgages began to reset at much higher rates than many borrowers could afford.

By mid-2006, home prices peaked, and the market slowed down. Then, when supply started to outpace demand, real estate prices plummeted. The combination of high-interest rates and falling home prices made it extremely difficult for mortgage-holders to make payments on their homes or sell the house (since their homes were worth less than they bought them for), so they defaulted.

As a result, banks were suddenly overwhelmed with loan losses on their balance sheets. The subprime mortgage crisis had begun.

Because of the overwhelming levels of derivative products, whose value was based on these loans, the collapse was soon felt beyond the housing industry. The defaults meant big derivative investors, like hedge fund managers, investment banks, and pension funds, saw the value of the investments nosedive.

Moreover, since CDOs didn’t trade on any exchanges, there was no way of selling them, so those who held them in their portfolios had to write off a considerable amount of their value.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

“The Big Short” and Michael Burry

Michael Lewis’s “The Big Short: Inside the Doomsday Machine” and the critically acclaimed 2015 film of the same name cleverly recount the few finance experts, including Michael Burry, to notice the instability in the U.S. housing market and predict its collapse.

In 2005, Wall Street hedge fund manager Michael Burry discovered that the various credit products, particularly MBSs, were full of high-risk subprime loans and would soon become unsustainable, i.e., borrowers would default on their loans rendering the derivatives worthless. This conclusion led him to short the housing market by throwing more than $1 billion of his investors’ money into credit default swaps (CDS) against subprime deals he saw as vulnerable. In short, he bet against the housing market.

His actions drew the interest of banker Jared Vennett, hedge-fund manager Mark Baum, and other opportunistic characters. Together, we observe these men making a fortune by exploiting the corrupt system and the impending economic downfall in America.

Recommended video: Michael Burry explains how he shorted the housing bubble

Wall Street crashes

The credit markets that funded the housing bubble quickly followed housing prices into a downturn as a credit crisis (breakdown of a financial system caused by a substantial disruption of normal cash movement) began unfolding in 2007.

In the coming months, the Fed and other central banks would take coordinated measures to provide billions in loans to the global credit markets, which were brought to a standstill as asset prices plummeted. At the same time, financial institutions struggled to estimate the value of the trillions of dollars worth of now-toxic debt securities sitting on their books.

In March, after suffering massive CDO losses, global investment bank Bear Stearns, a pillar of the stock market that dated to 1923, collapsed and was acquired by JPMorgan Chase (JPM) for $10 per share.

By the summer of 2008, the financial sector was in shambles. IndyMac Bank became one of the largest banks ever to fail in the U.S., and the U.S. government took over Fannie Mae and Freddie Mac.

Ultimately September 2008, with the bankruptcy of Lehman Brothers, the country’s fourth-largest investment bank, marked the climax of the subprime mortgage crisis, as panicked banks stopped lending almost entirely, and the global banking system became short of funds.

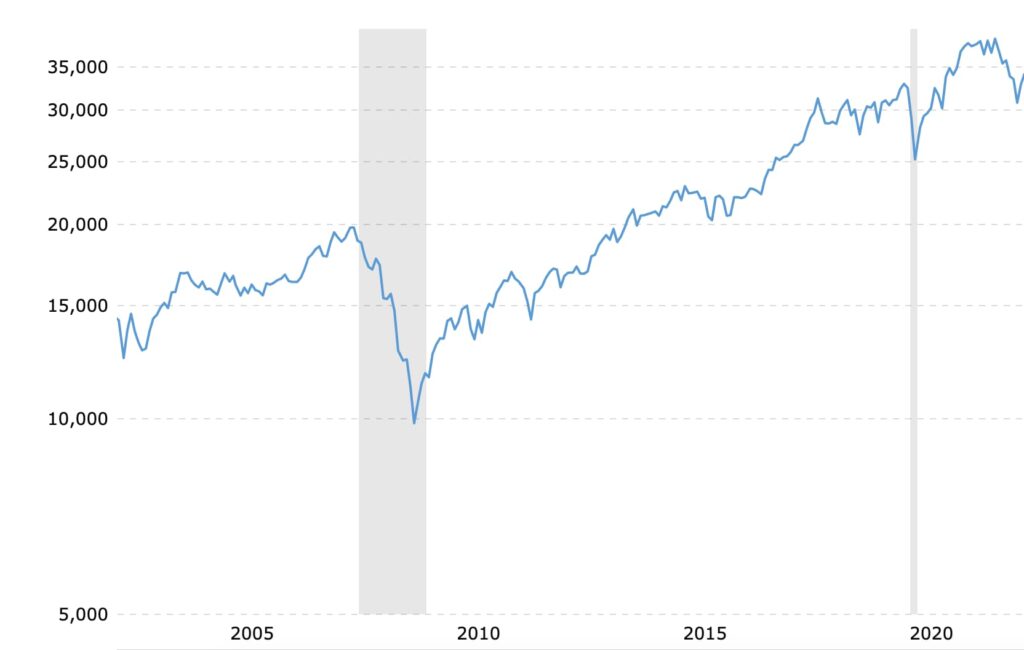

Wall Street crashed on September 29, 2008, with the Dow Jones Industrial Average (DJIA) falling by 777.68 points in intraday trading. The collapse was followed by an 18-month bear market that lasted until March 9, 2009, where the Dow experienced a drop of more than a half, to 6,594.44.

So although a stock market crash can cause a recession (e.g., the 1929 stock market crash), it had already begun in this case, making a bad situation much, much worse.

The Great Recession response

Although widely credited with preventing even more significant damage to the economy, the Federal Reserve’s aggressive monetary policies in reaction to the recession have also been criticized for prolonging the time it took the overall economy to recuperate and laying the groundwork for subsequent recessions.

Along with the wave of liquidity by the Fed, the U.S. Federal government embarked on a massive fiscal policy program to stimulate the economy, creating two key programs aimed at providing emergency assistance: Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act.

Let’s look at the Fed’s and the government’s policies to tame the recession.

Quantitative easing measures

The Federal Reserve dropped a key interest rate to nearly zero to boost liquidity and, in an unprecedented initiative, supplied banks with a staggering $7.7 trillion of emergency loans in a policy known as quantitative easing (QE).

As a result, the Fed’s balance sheet increased with bonds, mortgages, and other assets. U.S. bank reserves grew to over $4 trillion by 2017, providing liquidity to lend those reserves and stimulate overall economic growth.

Troubled Asset Relief Program (TARP)

As part of the Emergency Economic Stabilization Act of 2008, on October 3, 2008, Congress established, and President George W. Bush signed into law the Troubled Asset Relief Program (TARP), which aimed to stabilize the country’s financial system, restore economic growth, and mitigate foreclosures by purchasing troubled companies’ assets and stock.

TARP initially gave the Treasury purchasing power of $700 billion; the Dodd-Frank Wall Street Reform and Consumer Protection Act (referred to as Dodd-Frank) later reduced the $700 billion authorization to $475 billion.

The TARP funds helped in five areas:

- $245 billion was used to buy bank preferred stocks as a way to stabilize them;

- $27 billion went to programs to increase credit availability;

- $80 billion went bail out the U.S. auto industry;

- $68 billion towards stabilizing AIG;

- $46 billion went to foreclosure-prevention programs, such as Making Home Affordable.

In December 2013, the Treasury wrapped up TARP, and the government concluded that its investments had earned more than $11 billion for taxpayers. Specifically, TARP recovered funds totaling $441.7 billion from $426.4 billion invested.

Why did the government bailout banks?

Secretary of the Treasury at the time, Henry Paulson, described the primary purpose of TARP to the House Financial Services Committee as protecting the financial system from collapse, saying: “The rescue package was not intended to be an economic stimulus or an economic recovery package.”

TARP is still seen as controversial today. Critics lament the program’s effect on housing markets, which remained depressed for years. In addition, some say it didn’t go far enough and that the government should have demanded an equity stake in the companies it was bailing out to control their future practices.

Instead, critics suggest that TARP’s no-strings loans essentially rewarded bad behavior, and with no oversight in place, many banks ended up using that money for beefy executive bonuses. For example, even though TARP provisions demanded that companies involved lose certain tax benefits, by 2009, bailed-out firms paid approximately $20 billion to bank employees, scornfully referred to as TARP bonuses.

There were advocates of laissez-faire economics (an economic system of free-market capitalism that opposes government intervention), suggesting the banks go bankrupt, their worthless assets be written off, and the economy would fix itself by having other companies purchase the good assets.

However, there were no companies or banks that could afford to buy out these banks. Even Citigroup (C), one of the banks that the government had hoped would bail out the other banks, required a bailout to keep going. Rather, most government funds were used to create the assets that allowed the banks to write down about $1 trillion in losses.

In fact, that is what Hank Paulson attempted to do with Lehman Brothers in September of 2008, letting them go bankrupt. The result, however, was market panic, creating a run on the ultra-safe money market funds and threatening to shut down all businesses’ cash flow. In short, the free market couldn’t solve the problem without government help.

Ultimately, TARP did not endear the government to the American public, which saw Wall Street reap benefits as average citizens struggled with debt, unemployment, and foreclosures in the wake of the Great Recession.

The American Recovery and Reinvestment Act (ARRA)

On February 17, 2009, Congress passed the American Recovery and Reinvestment Act (also referred to as the “stimulus package of 2009”, the Recovery Act, or Obama stimulus). The stimulus plan consisted of $787 billion in spending (later raised to $831 billion), aiming at countering the job losses associated with the recession.

Other initiatives included providing temporary relief programs for those most affected by the recession and investing in infrastructure, education, healthcare, and renewable energy.

The aftermath of the Great Recession

Following these policies, the economy slowly recovered. Real GDP bottomed out in 2009 Q2, falling 4.3% from its peak in 2007 Q4, and regained its pre-recession peak in 2011 Q2, three and a half years after the initial onset of the official recession. In addition, financial markets recovered as the flood of liquidity washed over Wall Street first and foremost.

The Dow, which had lost more than half its value from its August 2007 peak, began to slowly recover in March 2009 and, four years later, in March 2013, broke its 2007 high.

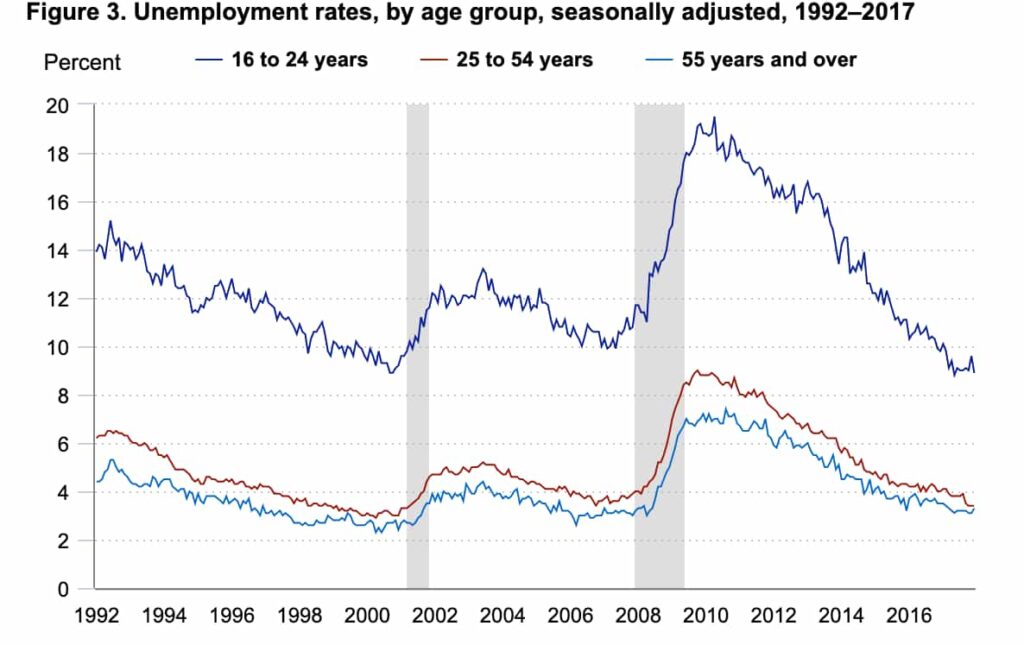

For workers and households, the outlook was less promising, particularly for Millennials who had just graduated and entered the workforce at the cusp of the crisis and landed in a terrible job market.

For example, as unemployment rates skyrocketed (it reached a high of 10% in October 2009), Millenials suffered the most. Unemployment rates for those aged 16-24 rose from 9.9% in May 2007 to a record 19.5% by April 2010, compared to 8.8% for 25-54-year-olds and 7.0% for 55 and older. And though by December 2017, unemployment had fallen to 8.9% for millennials, the damage had already been done.

Millennials still bear the brunt of the Great Recession. Though they are better educated than prior generations, Millenials have decreased savings and heavy student loan debt, something their parents never had to confront.

As a result, they have less wealth than previous generations at a comparable age. Overall, millennials earn 20% less than baby boomers did at the same stage of life, according to “The Emerging Millennial Wealth Gap,” a recent report from the nonprofit, nonpartisan think tank New America.

In conclusion

The Great Recession is one of U.S. history’s most severe economic downturns. Indeed a fair bit of similarities can be drawn to the Great Depression as both involved reckless speculation, cheap credit, and too much debt in asset markets, i.e., the housing market in 2008 and Wall Street in 1929.

Although the subprime mortgage meltdown was the immediate cause, a mix of factors and participants precipitated the financial crisis. Still, human behavior and greed ultimately drove the demand, supply, and investor appetite for these types of loans.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about the Great Recession

How did the financial crisis look in numbers?

- The Recession lasted 19 months;

- The net worth of U.S. households declined, erasing $19.2 trillion in wealth;

- GDP fell 4.3%;

- The unemployment rate peaked at 10% in October 2009; rates were even higher among Black and Hispanic households as well as Millenials;

- 8.8 million jobs lost;

- The U.S. lost $7.4 trillion in stock wealth, or $66,200 per household, from July 2008 to March 2009;

- 8 million home foreclosures;

- Employee-sponsored retirement account balances declined 25% or more in 2008;

- Failure rates for ARMs climbed to nearly 30% by 2010.

Who is to blame for the Great Recession of 2008?

The primary blame for the Great Recession could be bestowed upon lax lending policies that allowed many consumers to borrow beyond their financial capabilities. But let’s not forget the predatory lenders who marketed homeownership to these individuals, as well as the investment firms who bought those bad mortgages and rolled them into bundles for resale to investors. Moreover, massive responsibility lies on the rating agencies who gave those derivative products triple-A ratings, making them appear safe.

What was the government's response to the financial crisis?

To address the financial crisis, the U.S. government introduced two key programs: the Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA). TARP, with a $700 billion fund, aimed to stabilize the banking sector, the auto industry, and prevent foreclosures by buying equity in struggling firms. ARRA, enacted in 2009, focused on economic stimulation through tax cuts, spending programs, loan guarantees, and extended unemployment benefits. These initiatives were central to the government’s strategy to mitigate the recession’s impact.

How did the Great Recession illustrate one of the weaknesses of a free enterprise economy?

The Great Recession highlighted a key weakness of a free enterprise economy: the potential for unchecked risk-taking and lack of regulation, especially in the financial sector. This period saw excessive risk-taking by financial institutions, largely driven by the pursuit of profit, and a lack of adequate regulatory oversight. The subprime mortgage crisis, which triggered the recession, exemplified how these factors can lead to widespread economic instability, revealing the vulnerability of a free enterprise system to financial crises when market forces are not balanced by sufficient regulatory safeguards.

What are the similarities and the differences between the Great Recession and the Great Depression?

The Great Depression and the Great Recession both involved significant economic downturns, but differed in severity, causes, and global impact. The Great Depression, triggered by the 1929 stock market crash, led to a decade-long worldwide economic slump, marked by extreme unemployment and deflation. In contrast, the Great Recession, sparked by the housing market collapse and financial system failures, had a shorter duration and was primarily concentrated in the financial sector. While both events led to regulatory reforms, the Great Recession’s impact was softened by quicker and more robust governmental interventions compared to the 1930s.

What are some of the best books on the Great Recession?

A few famous books analyzing the Great Recession are “The Big Short” by Michael Lewis, which offers an engaging look at those who profited from the housing market crash; “Too Big to Fail” by Andrew Ross Sorkin, detailing the urgent efforts to save the financial system; and “All the Devils Are Here” by Bethany McLean and Joe Nocera, providing a comprehensive examination of the crisis’s roots and culprits.

To better understand the Great Recession, take a look at our other guides on the topic: