This guide will examine mortgage-backed securities, what they are and how they work, as well as the risks involved with this particular investment product. Furthermore, we will also delve into the pitfalls of the MBS market leading up to the eventual 2008 housing crash and how it ultimately changed the housing market.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

What are mortgage-backed securities?

As a result, a bank can grant mortgages to its clients and then sell them at a discount to be bundled as MBSs to investors as a type of collateralized bond. The bank reports the sale as a plus on its balance sheet and risks nothing if the homebuyer defaults on their loan.

In return, the investor gets the rights to the value of the mortgage, including interest and principal payments made by the borrower. However, if the homeowner defaults, the investor who paid for the mortgage-backed security won’t get paid, which means they could lose money. Therefore, an MBS is only as sound as the mortgages that back it up, a fact that became painfully evident during the subprime mortgage meltdown of 2007-2008.

Typical buyers of MBS include individual investors, corporations, and institutional investors. Two primary types of MBSs are pass-throughs and collateralized mortgage obligations (CMO). An MBS is traded on the secondary market and can be bought and sold through a broker. The minimum investment varies between issuers.

Today, an MBS can only be issued by a government-sponsored enterprise (GSE) or a private financial company to be sold on the markets. In addition, the mortgages have to originate from a regulated and authorized financial institution. Moreover, the MBS must have received one of the top two ratings issued by an accredited credit rating agency.

Beginners’ corner:

- What is Investing? Putting Money to Work

- 17 Common Investing Mistakes to Avoid

- 15 Top-Rated Investment Books of All Time

- How to Buy Stocks? Complete Beginner’s Guide

- 10 Best Stock Trading Books for Beginners

- 15 Highest-Rated Crypto Books for Beginners

- 6 Basic Rules of Investing

- Dividend Investing for Beginners

- Top 6 Real Estate Investing Books for Beginners

- 5 Passive Income Investment Ideas

History of mortgage-backed securities

Following The Great Depression of the 1930s, when the government established the Federal Housing Administration (FHA) to assist in rehabilitating and constructing residential houses. In addition, the agency aided in developing and standardizing the fixed-rate mortgage and popularizing its usage.

Then, in 1938, the government created Fannie Mae, a government-sponsored enterprise, to create a liquid secondary market for these mortgages and thereby free up capital from banks to generate more loans, mainly by buying FHA-insured mortgages.

Fannie Mae was later split into Fannie Mae and Ginnie Mae to support the FHA-insured mortgages, Veterans Administration, and Farmers Home Administration-insured mortgages. Finally, in 1970, the government created another agency, Freddie Mac, to perform similar functions to Fannie Mae’s.

MBSs allowed non-bank financial institutions to enter the mortgage business. Before MBSs, only banks had significant enough deposits to make long-term loans or the capacity to wait until these loans were repaid decades later.

The invention of MBSs meant lenders immediately got their cash back from investors on the secondary market, freeing up funds to lend to more homeowners. As a result, the number of lenders skyrocketed. For example, some offered mortgages that didn’t look at a borrower’s job or assets, creating more competition for traditional banks, which, in turn, had to lower their standards to compete.

Unfortunately, MBSs were not regulated. The federal government regulated banks to protect their depositors, but those rules didn’t apply to MBSs and mortgage brokers. So though bank depositors were safe, MBS investors were not covered.

How do mortgage backed securities work?

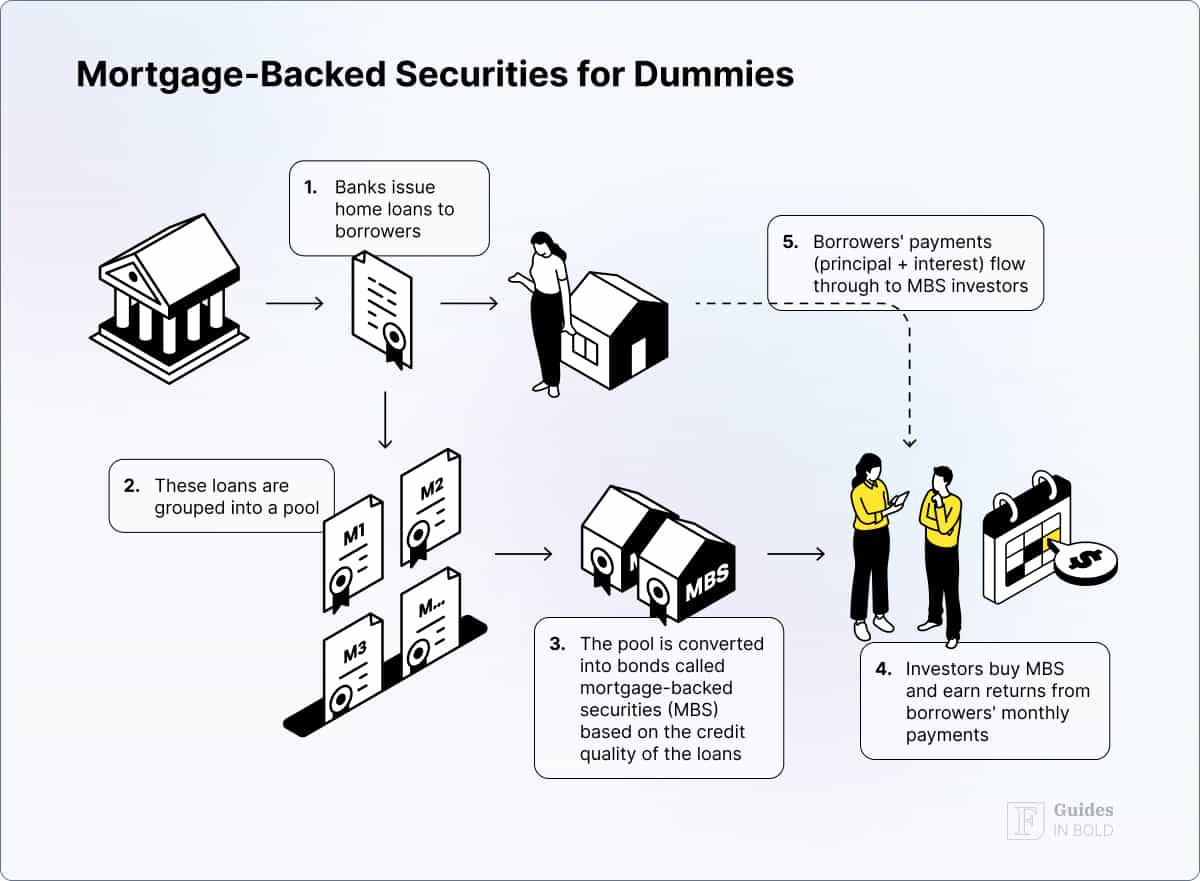

First, a bank or a financial institution provides a home loan to one of its customers. It then sells that loan to an investment bank. Finally, it uses the money received from the investment bank to make new loans.

Next, the investment bank takes the original loan and adds it to a bundle of mortgages based on the credit quality attached to the underlying security and markets them to investors.

The investors then buy the MBSs (similar to a bond) and collect monthly income (principal and interest) while holding them. So, in principle, if the customer pays off their mortgage, the MBS investor profits.

Who issues mortgage-backed securities?

The majority of mortgage-backed securities are offered by an entity of the U.S. government, such as:

- The Government National Mortgage Association (Ginnie Mae);

- The Federal Home Loan Mortgage Corporation (Freddie Mac);

- The Federal National Mortgage Association (Fannie Mae).

As a result, they are often classified together in what is known as government-supported mortgage-backed securities.

Government National Mortgage Association (Ginnie Mae)

The Government National Mortgage Association (GNMA), commonly referred to as Ginnie Mae, is a federal government corporation that secures the principal and interest payments on mortgage-backed securities issued by approved lenders. Ginnie Mae’s goal is to ensure affordable home loans for underserved consumers in the mortgage market.

Federal National Mortgage Association (Fannie Mae)

The Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, is a publically owned government-sponsored enterprise (GSE) established in 1938 by Congress during the Great Depression as part of the New Deal.

It was formed to stimulate the housing market by making more mortgages available to moderate-to low-income borrowers. Rather than providing loans, it backs or guarantees them in the secondary mortgage market.

Federal Home Loan Mortgage Corporation (Freddie Mac)

The Federal Home Loan Mortgage Corp. (FHLMC), familiar as Freddie Mac, is a publically owned, government-sponsored enterprise (GSE) chartered in 1970 by Congress to keep money flowing to mortgage lenders to support homeownership and rental housing for middle-income citizens. The role of Freddie Mac is to purchase loans from mortgage lenders, then merge them and sell them as MBSs.

Fannie Mae and Freddie Mac are both publicly traded GSEs, with their primary difference being that Fannie Mae buys mortgage loans from major retail or commercial banks, while Freddie Mac gets its loans from smaller banks.

Fannie Mae and Freddie Mac were bailed out by the U.S. government following the financial crisis and delisted from the NYSE. Today, Fannie Mae’s and Freddie Mac’s shares are traded over-the-counter (OTC), meaning you can’t buy them on a major stock exchange.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Types of mortgage-backed securities

There are three basic types of mortgage-backed security:

- Pass-through MBS;

- Collateralized mortgage obligation (CMO);

- Collateralized debt obligation (CDO).

Pass-through MBS

The simplest MBS is the pass-through mortgage-backed security. Pass-throughs are constructed as trusts in which mortgage payments are received and passed through as principal and interest payments to bondholders. They typically come with stated maturities of five, 15, or 30 years.

However, the average life of a pass-through may be less than the stated maturity depending on the principal payments on the mortgages that assemble the pass-through.

Collateralized mortgage obligation (CMO)

A collateralized mortgage obligation (CMO) is a financial product backed by a pool of mortgages bundled together and sold as an investment. CMOs generate cash flow as borrowers repay the mortgages that act as collateral on these securities. This, in turn, is distributed to investors as principal and interest payments based on predefined agreements.

Collateralized mortgage obligations are organized by slicing a pool of mortgages into similar risk profiles known as tranches. Tranches are given different credit ratings and generally have different principal balances, interest rates, maturity dates, and the potential for repayment defaults.

The less risky tranches have more certain cash flows and a lower degree of exposure to default risk, while riskier tranches have more uncertain cash flows and more significant exposure to default risk. The elevated level of risk, however, is compensated with higher interest rates.

Collateralized mortgage obligations are influenced by interest rate changes as well as economic conditions, like foreclosure rates, refinance rates, as well as the rates and amounts at which properties are sold. Therefore, each tranche has a different size and maturity date, and bonds with monthly coupons (with principal and interest rate payments) are issued against it.

Collateralized mortgage obligation example

Conversely, if thousands of people cannot make their mortgage payments and go into foreclosure, the CMO loses money and cannot pay the investor.

Collateralized debt obligation (CDO)

Like CMO, collateralized debt obligation (CDO) is a complex structured finance product backed by a pool of loans (in this case, various types, e.g., mortgages, credit card debt, student loans) and other assets sold to institutional investors by investment banks.

CDOs, too, generate cash flow as lenders repay the loans that act as collateral on these securities. The principal and interest payments are then redirected to the investors in the pool. If the underlying loans fail, the banks transfer most of the risk to the investor, typically a large hedge fund or a pension fund.

Banks slice CDOs into various risk levels or tranches. The least risky tranches have more certain cash flows and a lower degree of exposure to default risk. At the same time, riskier tranches have more uncertain cash flows and greater exposure to default risk but offer higher interest rates to attract investors.

How are CDO tranches structured?

Each tranche has a perceived (or stated) credit rating, which measures its risk of default (the failure to make required interest or principal repayments on a loan or financial instrument).

The top tier rating is usually ‘AAA‘ rated senior tranche. The middle tranches are typically called mezzanine tranches and generally carry ‘AA‘ to ‘BB‘ ratings, and the lowest or unrated tranches are referred to as the equity tranches. Each rating determines the amount of principal and interest each tranche receives.

The senior tranche is the first to soak up cash flows and the last to absorb loan defaults or missed payments. Therefore, it has the most predictable cash flow and is usually thought to carry the least risk. In contrast, the lowest-rated tranches usually only receive principal and interest payments after all other tranches are paid. On top of this, they are first in line to absorb defaults and late fees.

CDOs can also be made up of a pool of prime loans, near-prime loans (called Alt.-A loans), risky subprime loans, or a combination of the above.

Additionally, some structures use leverage and credit derivatives that can render even the senior tranche risky. These structures can become synthetic CDOs backed merely by derivatives and credit default swaps made between lenders and in the derivative markets.

Watch the video: Ryan Gosling (The Big Short) explains the structure of a basic mortgage bond:

Commercial mortgage-backed securities (CMBS) vs. residential mortgage-backed security (RMBS)

Mortgage-backed securities come in two main varieties: commercial mortgage-backed securities (CMBS) and residential mortgage-backed securities (RMBS).

CMBS are backed by large commercial loans, referred to as CMBS or conduit loans. RMBS are backed by residential mortgages (e.g., home equity loans, Federal Housing Administration (FHA) insured loans).

While the underlying loans backing RMBS are strictly residential real estate, most often single-family homes, the underlying loans that are pooled into CMBS include loans on income-producing commercial properties such as apartment buildings, factories, hotels, office buildings, shopping malls, etc.

Both CMBS and RMBS are structured into various tranches based on the risk of the loans. The senior tranches get paid off first in the case of a loan default, while lower tranches will be compensated later (or not at all) should the borrowers fail to meet payments.

Mortgage-backed securities ETFs

Mortgage-backed securities exchange-traded funds (ETFs) that focus on securities provide an opportunity for fixed-income investors to get exposure to this market. Three examples of ETFs that invest in mortgage-backed securities are:

- iShares MBS Bond ETF: The iShares MBS Bond ETF (MBB) is a solid option for investors wanting to invest in fixed-rate mortgage pass-through securities issued by the housing GSEs: Fannie Mae, Ginnie Mae, and Freddie Mac. The fund tracks the performance of the Bloomberg U.S. MBS Index, and the majority of the fund’s holdings are concentrated in 30-year fixed-rate mortgages;

- SPDR Portfolio Mortgage Backed Bond ETF: The SPDR Portfolio Mortgage Backed Bond ETF (SPMB) also aims to match the price and return performance of its benchmark, the Bloomberg U.S. MBS Index, by investing in the securities backed by the housing GSEs;

- Vanguard Mortgage-Backed Securities ETF: The Vanguard Mortgage-Backed Securities ETF (VMBS) follows the performance of the Bloomberg U.S. MBS Float Adjusted Index. The ETF comes with moderate interest rate risk, with a dollar-weighted average maturity of three to 10 years.

Mortgage-backed securities and the global financial crisis

Low-quality MBSs were among the factors that led to The Great Recession of 2008. Even though the U.S. federal government regulated the financial institutions that assembled MBSs, there was a lack of laws governing them directly.

The absence of regulation meant that financial institutions could get their money instantly by selling MBS products immediately after making the loans. Still, investors in MBS were practically not protected at all, and if the borrowers of mortgages defaulted, there wasn’t a concrete way to compensate MBS investors.

Ultimately, investors were more likely to focus on the steady revenue offered by CMOs and other MBS securities rather than the underlying mortgages’ health. As a result, many purchased CMOs full of subprime mortgages, adjustable-rate mortgages, mortgages held by lenders whose income wasn’t verified, and other risky mortgages with a high likelihood of default.

As the market attracted various mortgage lenders, including non-bank financial institutions, traditional lenders were forced to lower their credit standards to compete in the home loan business. Simultaneously, the U.S. government pressured banks to extend mortgage financing to higher credit risk borrowers, creating massive amounts of mortgages with an increased risk of default. In short, many borrowers got into loan obligations that they could not afford.

However, with a steady supply of, and increasing demand for, mortgage-backed securities, Freddie Mac and Fannie Mae aggressively supported the market by issuing ever more MBS. But unfortunately, the MBS created were increasingly low-quality, high-risk investments.

And though rising housing prices made mortgages look like fail-proof investments, market and economic conditions instituted a spike in foreclosures and payment risks that financial models did not accurately predict.

Eventually, when mortgage borrowers began to default on their loans, it led to a domino effect of collapsing the housing market and wiping out trillions of dollars from the U.S. economy. Moreover, the impact of the sub-prime mortgage crisis spread to other countries around the globe.

Further reading

The state of mortgage-backed securities today

Even though mortgage-backed securities were at the crux of the financial crisis of 2007-2009, they continue to be an essential part of the economy today because they serve real needs and provide tangible benefits to participants across the mortgage and housing industries.

Firstly, not only does securitization of mortgages provide increased liquidity for investors, lenders, and borrowers, but it also offers a way to support the housing market. A strong housing market often bolsters a strong economy and helps drive growth.

After the housing crash, the U.S. government increased regulations in several areas, including residential MBSs. As a result, MBSs must now provide disclosures to investors on several issues. In response to the new requirements, however, there are fewer registered MBSs except those offered by Fannie Mae and Freddie Mac.

Finally, CDOs have returned after becoming unpopular for a few years post-crisis with the assumption that Wall Street has learned from its mistakes and will question the value of MBSs rather than recklessly buying them.

Pros and cons of mortgage-backed securities

Pros

- Handsome returns: Mortgage-backed securities generally offer higher yields than government bonds. However, though lower tranches provide higher interest rates, they also carry elevated credit and prepayment risk, meaning the eventual outcome could be lower than initially expected;

- Independent: Less correlated to stocks than other high yield fixed income securities;

- Credit quality: Credit risk is influenced by the number of borrowers in the pool of mortgages who default on their loans. For mortgages issued by federal agencies or GSEs, credit risk is considered minimal;

- Liquidity: MBSs are part of the system that helps borrowers access capital more cheaply.

Cons

- Credit and default risk: While MBSs backed by GNMA have a low risk of default, there is some default risk for MBS backed by FHLMC and FNMA and an even higher risk of default for securities issued by private agencies. Before investing, investors should inspect the characteristics of the MBS’s underlying mortgage pool (e.g., borrower creditworthiness). Furthermore, the credit risk of the issuer itself may also be a factor, depending on the legal structure and entity that owns the underlying mortgages;

- Prepayment risk: There is a chance, mainly when interest rates are falling, that borrowers will make higher-than-required monthly loan payments or pay their mortgages off by refinancing. As a result, the principal retained in the bond declines faster than initially projected, shortening the average life of the bond. However, prepayment risk can somewhat be reduced by pooling together more mortgages since each prepayment would have a more negligible effect on the total pool;

- Changing cash flow: Because prepayment risk is highly likely in an MBS case, revenue can be estimated but is subject to change. Moreover, in the case of CMOs, when prepayments occur more frequently than expected, the average life of a security is shorter than initially estimated. While some CMO tranches are designed to minimize the effects of variable prepayment rates, the average life is always only an estimated contingent on how closely the actual prepayment speeds of the underlying mortgage loans match the assumption;

- Extension risk: There is a risk of homeowners deciding not to make prepayments on their mortgages to the extent initially anticipated. This usually occurs when interest rates rise, giving homeowners little incentive to refinance their fixed-rate mortgages, resulting in a security that locks up assets for longer than expected and delivers a lower coupon since the amount of principal repayment is reduced. As a result, in a period of rising market interest rates, the price declines of MBSs would be further highlighted due to the declining coupon;

- Interest rate risk: Generally, bond prices in the secondary market increase when interest rates decline and vice versa. However, because of prepayment and extension risk, the secondary market price of an MBS (especially a CMO) will sometimes grow less than a typical bond when interest rates fall but may drop more when interest rates rise. Thus, these securities may have greater interest rate risk than other bonds;

- Low liquidity for CMOs: MBSs are typically considered a liquid product, with active trading by dealers and investors. However, CMOs can be less liquid than other MBSs due to the specific attributes of each tranche. Therefore, before purchasing a CMO, investors should possess a high level of expertise to understand the implications of tranche specification.

Conclusion

To sum up, the creation of mortgage-backed securities completely revolutionized the housing, banking, and mortgage market. By restructuring a collection of illiquid loans into tradeable securities, MBSs allowed for bank funds to be freed up and created more demand to lend money, letting more people buy homes.

However, due to inadequate regulations, soaring housing prices, and increasing demand, the market of MBSs slipped out of control during the real estate boom, as banks got greedy and didn’t take the time to confirm borrowers’ creditworthiness. As a result, people got into mortgages they couldn’t afford.

Still, regardless of the state of the economy, MBSs are likely to exist in some form. For example, if loans cannot be sliced up into tranches, the result will be tighter credit markets with higher borrowing rates. So as long as there is a pool of borrowers and lenders, financial institutions will be willing to take risks to capitalize on these cash flows, with each new decade potentially bringing out new structured products with new challenges for investors and the markets.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about mortgage-backed securities

What are mortgage-backed securities?

Mortgage-backed security (MBS) is a bond secured by a collection of mortgages bought from the issuing banks. The investor who buys mortgage-backed securities is essentially lending money to home buyers.

How do mortgage-backed securities work?

In mortgage-backed securities, banks act as intermediaries. They issue mortgages to homebuyers and then sell these mortgages to investors, packaging them into MBSs. Investors purchasing these securities gain rights to the mortgage value, including the borrower’s monthly payments of interest and principal. The investors profit as long as the borrowers continue to pay off their mortgages.

What are the types of mortgage-backed securities?

Mortgage-backed securities come in three main types: pass-through MBS, collateralized mortgage obligations (CMOs), and collateralized debt obligations (CDOs). Both CMOs and CDOs are grouped into risk-similar mortgage pools called tranches, which have varying credit ratings. Tranches differ in principal balances, interest rates, maturity dates, and default risk potential. Less risky tranches offer more stable cash flows and lower default risk, while riskier tranches, offering higher interest rates to compensate, face greater uncertainty in cash flows and higher default risk.

Who issues mortgage-backed securities?

Most mortgage-backed securities are offered by an entity of the U.S. government, such as Ginnie Mae, Freddie Mac, and Fannie Mae, and are often classified together in what is known as government-supported mortgage-backed securities.

Are mortgage-backed securities safe?

The risk applies to MBS as to other financial instruments. Two distinct risks associated are prepayment risk and extension risk. Others include default, interest rate, credit, and reinvestment risk.

How to buy mortgage backed securities?

You can invest in individual mortgage-backed securities through an online broker, for example, Fidelity, Interactive Brokers, or TD Ameritrade, or invest in mortgage-backed securities ETFs.

What are commercial mortgage-backed securities?

Commercial mortgage-backed securities (CMBS) are a type of fixed-income investment product. They are secured by mortgages on commercial properties rather than residential real estate. These securities are created by pooling various commercial mortgage loans and selling them to investors in the form of bonds.

Why did banks believe that mortgage-backed securities protected them from defaults?

Banks believed that mortgage-backed securities protected them from defaults because these securities distributed the risk of borrower defaults across a wide pool of investors. By bundling numerous mortgages into a single MBS, the risk of any single borrower defaulting was diluted across the entire pool. Additionally, MBS often used tranches, where the risk of default was layered, with some investors accepting higher risk for potentially higher returns, while others had more secure, lower-yielding investments. This structure was perceived to mitigate the impact of defaults on any single investor or the issuing bank.

How to short mortgage-backed securities?

To short mortgage-backed securities, investors follow a strategy of selling securities they don’t own with the expectation of buying them back later at a lower price, thereby profiting from the price difference. Shorting MBS involves risks like market volatility, potential unlimited losses, borrowing costs, timing, liquidity challenges, and regulatory considerations. It’s crucial to understand these risks and have a strategy for managing them.

Are mortgage backed securities derivatives?

Mortgage-backed securities are not derivatives. They are a type of asset-backed security that is secured by a collection of mortgages. Essentially, an MBS is a bond secured by home loans. Derivatives, on the other hand, are financial instruments whose value is derived from the value of an underlying asset, index, or interest rate. MBS are backed by tangible assets (the mortgages themselves) and represent a direct claim on the cash flows from these mortgages, whereas derivatives are based on the performance of these underlying assets without necessarily having a direct claim on them.

Who are the largest holders of MBS?

The largest holders of mortgage-backed securities (MBS) are primarily government-sponsored enterprises (GSEs) and major financial institutions. The Federal Reserve is the single largest holder, followed by GSEs like Fannie Mae and Freddie Mac. Large commercial banks and institutional investors, such as mutual funds and insurance companies, also hold significant amounts of MBS.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.