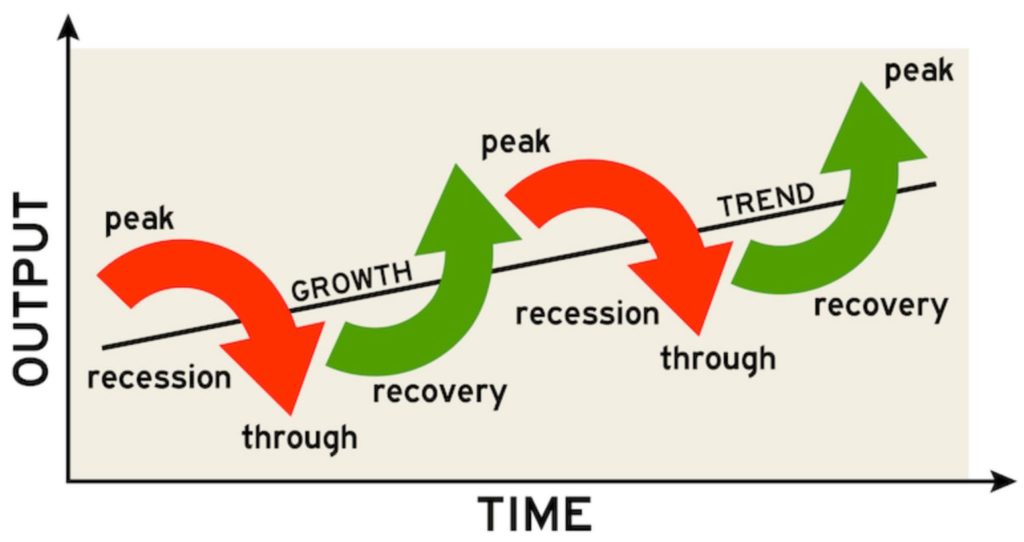

Markets are cyclical, meaning that the current trends will not last forever. Shuffling downturns, recoveries, and surges make the financial world a volatile place, sometimes less, sometimes more. Rebalancing your portfolio to keep track of the changing market circumstances is paramount to any long-term investing strategy. Today, we will elaborate on how to realign your investment portfolio, along with some tips and tricks to help you navigate market volatility.

Why you should realign your portfolio

A sound investing portfolio is diversified. In other words, any serious investor has multiple components as parts of their holdings, often mixing various assets such as stocks, bonds, mutual funds and ETFs, or even cryptocurrency.

| Asset | Investment type and span | Risk |

| Stocks | Active, long- and short- term | Medium-high |

| Index funds and ETFs | Long-term growth | Low-medium |

| REITs | Long-term, passive income | Medium |

| Bonds | Long-term, fixed-income | Low |

| Cryptocurrency | Alternative, usually short-term | Very high |

Investment assets come with various levels of risk, timespans, and potential returns. Investors should always diversify their portfolios to find the sweet spot between a comfortable level of risk and attractive potential returns over a planned period.

However, market volatility complicates things.

Let’s imagine a simple portfolio comprising 70% stocks and 30% bonds. However, if the stock market goes bullish, your stocks surge in price, and the composition shifts to 75% stocks and 25% bonds. Although having a part of your portfolio perform well is excellent news, your portfolio’s total risk level has increased, and preserving the previous status requires selling the excess shares.

On the other hand, imagine the stock market went bearish instead. The price of your stocks has fallen, and suddenly, the value of your portfolio has shifted to 65% stocks and 35% bonds. Casual investors might succumb to fear and decrease their stock positions. However counterintuitive it might seem, this is an ideal opportunity for seasoned investors to buy stocks to return to the desired ratio.

The emotional and psychological pressure of selling well-performing assets and buying losers can be severe. However, the foreknowledge that the market is cyclical in nature and that the economic phase is guaranteed to change given enough time can help you steady your nerves.

Stick to your portfolio goals

It is crucial that you set your investing goals before you engage in portfolio realignment.

There are a couple of factors that can influence your golden portfolio ratio:

- Age: The point in life you find yourself in when realigning your portfolio is important as it determines how long you can wait for the investment to bear fruits. If you are 25, you have time to afford to invest in riskier, more long-term assets such as stocks. Likewise, if you are 75, you should prefer more conservative investments like fixed-term bonds. Many investors adhere to the “100 minus your age“ equity ratio, which would have a 25-year-old’s portfolio contain 75% stocks and a 75-year-old’s portfolio contain 25% stocks. However, not all agree on the effectiveness of such a ratio. Therefore, it should not be a rule but a guideline, as comfortable risk levels depend on the individual;

- Risk: Higher risk brings higher potential rewards but also tends to increase the frequency of events in which you lose money. One of the most challenging tasks in investing is to find the risk level you are comfortable with. Age does play a role, but being young does not necessarily mean being in love with risk, and vice versa;

- Goals and timetables: Most long-term investing cases have a grand retirement plan in mind, which implies a conservative take on your portfolio with decades for the portfolio to bear fruit. However, it is also possible you need the funds more quickly, perhaps in two years, which can limit your reliance on bonds or eliminate them from the equation. Make sure you consider not only how much money but also how much time you can afford.

How often should you rebalance your portfolio?

Reshuffling your assets has to be planned and regular, but not too frequent, as every realignment comes with fees and costs. Consider the following cases:

- Regularly, once per year: Pick a date to do it regularly, for example, the day after you do your taxes or on your birthday;

- Whenever the asset ratio shifts by a certain percentage: Our previous example was 5%, but you can also stick with 3%,10%, or any other percentage you like;

- DO it once per year, but only if the allocation ratio has changed by a certain percentage, which is a mix of both previous solutions.

What is the 5/25 rule for rebalancing?

Larry Swedroe, a financial advisor and investor, has come up with a 5/25 rule, which dictates that you should realign your portfolio in either absolute 5% or relative 25%:

- Absolute 5% for simpler allocations (20% or greater): If your target asset ratio is like in our previous example, 70% in stocks and 30% in bonds, you should realign your portfolio if these percentages reach either 75% or 65% in stocks;

- Relative 25% (for allocations less than 20%): If you hold 70% in stocks, 20% in bonds, and 10% in crypto, you should realign your portfolio if the crypto ratio changes by 25% relative to its position, or this case +/- 2.5% (25% of 10%).

How to rebalance your investment portfolio in volatile times – the bottom line

Viable long-term strategies require planned portfolio rebalancing without emotions, which furthers the desired investing objective. Consider realigning your portfolio like going to a car mechanic: it is far better to do it regularly and have your car (portfolio) in perfect condition than to visit them once your car (portfolio) crashes.

Carefully consider the risk of each portfolio component and balance it with your desired returns. Once thresholds are breached, balance the shifted results of market volatility. However, remember that your ideal portfolio ratio can also change over time, whether you grow more risk-weary or risk-friendly.

Finally, consider the cost of every realignment: transaction fees, maintenance costs, and other small payments can compound to reduce or even eliminate your gains.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.