Wall Street analysts remain bullish on Meta Platforms (NASDAQ: META) stock despite the social media giant experiencing volatility in 2026.

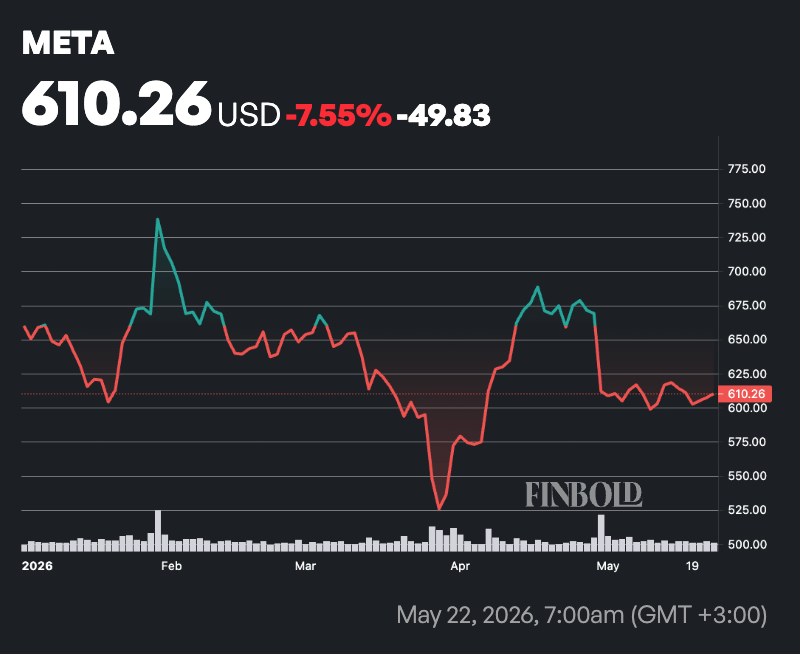

So far this year, META stock has fallen more than 6%. The shares closed the last session at $610, up about 0.5% on the day.

Despite the weakness, Meta continues to be supported by strong fundamentals, with analysts betting that the company’s aggressive artificial intelligence (AI) investments will pay off over the long term.

Notably, Meta shares pulled back after the company released its first-quarter 2026 results on April 29. The company reported revenue of $56.31 billion, up 33% year-over-year, while earnings per share came in at $10.44.

Daily active users across its family of apps reached 3.56 billion. However, the stock declined after Meta raised its full-year capital expenditure guidance to between $125 billion and $145 billion to accelerate AI infrastructure expansion.

Despite the pullback, analysts largely viewed the dip as a buying opportunity. Meta’s advertising business, which generates nearly all of its revenue, continues to benefit from AI-driven improvements in ad targeting, creative generation, and campaign performance, helping boost ad impressions and pricing.

Looking ahead, Meta guided for second-quarter 2026 revenue of between $58 billion and $61 billion. While heavy spending on AI infrastructure is expected to pressure near-term margins and free cash flow, successful monetization of its Llama models and Meta AI features could support long-term growth.

Key risks include elevated capital expenditures, regulatory scrutiny over antitrust, privacy, and content moderation issues, as well as intense competition in AI and social media.

Wall Street analysts Meta stock outlook

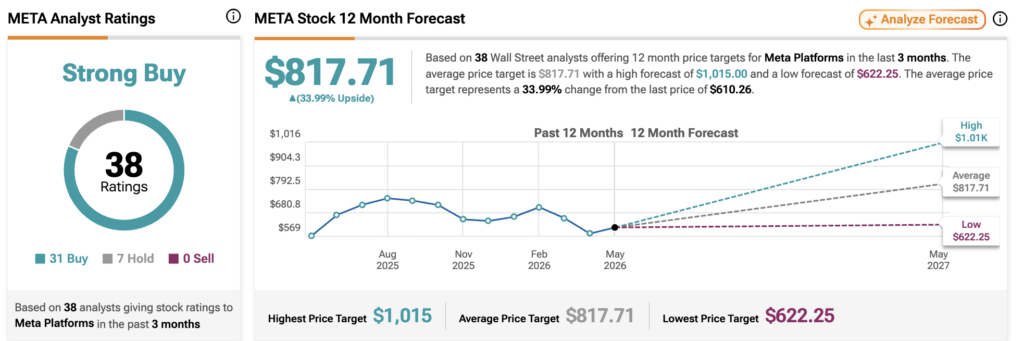

Regarding the META stock outlook, analysts at TipRanks have assigned the stock a ‘Strong Buy’ consensus rating. The average 12-month price target stands at $817.71, implying a potential upside of 33.99%. The highest forecast is $1,015, while the lowest is $622.25.

The outlook is based on ratings from 38 Wall Street analysts over the past three months. Among them, 31 rate Meta shares as ‘Buy’, seven recommend ‘Hold’, and none carry a ‘Sell’ rating.

Wells Fargo analyst Ken Gawrelski slightly lowered Meta’s price target to $765 from $770 while maintaining an ‘Overweight’ rating, signaling continued confidence in the company’s AI strategy. The analyst said Meta remains well-positioned to benefit from growing investor optimism around companies monetizing large AI compute investments, even though it does not directly sell cloud services. Gawrelski also pointed to accelerating AI infrastructure spending.

On the other hand, Mizuho lowered Meta’s price target to $835 from $850 while maintaining an ‘Outperform’ rating, saying the company still has strong long-term potential despite recent stock weakness. The firm expects upcoming AI product launches to provide more clarity on Meta’s large language model strategy and monetization plans, particularly as the company focuses on consumer-facing AI tools while rivals target enterprise customers. Mizuho was encouraged by rising Meta AI usage following the Muse Spark launch but said the company must show clearer product progress, stronger adoption, or tighter control over spending and capital expenditures before its second-quarter earnings report.