Wall Street analysts are projecting that healthcare giant UnitedHealth (NYSE: UNH) stock is likely to see further momentum over the next 12 months.

Over the past month, UNH shares have rallied 20% and were trading at $389 at press time after ending the last session down nearly 2%. Year-to-date, the stock has gained 15%, continuing its recovery following a difficult 2025.

The momentum comes as investors digest Berkshire Hathaway (NYSE: BRK.A) fully exiting its position in UNH after selling roughly 5 million shares in the first quarter of 2026 under CEO Greg Abel. The move briefly pushed UNH shares down 2% to 3% before a partial recovery.

Despite the pressure, UnitedHealth posted stronger-than-expected first-quarter results, with revenue rising 2% year over year to $111.7 billion and adjusted EPS reaching $7.23, ahead of estimates.

The company also raised its full-year 2026 adjusted EPS guidance above $18.25 as improving margins and continued growth at Optum helped offset concerns around medical costs and Medicare Advantage trends.

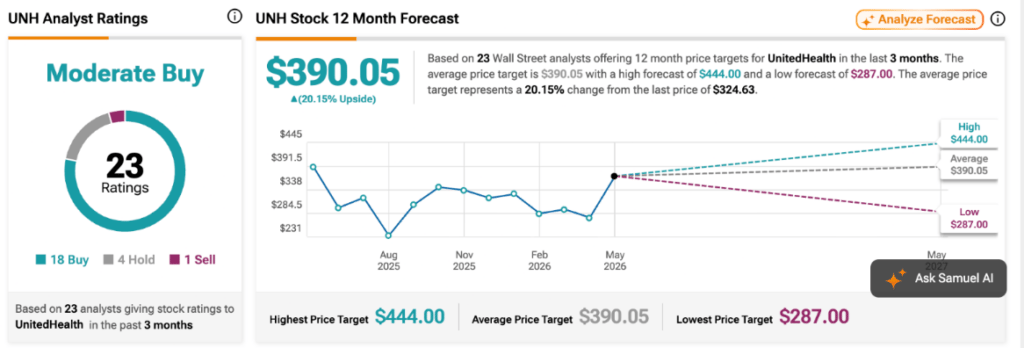

Meanwhile, analysts remain cautiously optimistic on UNH despite recent volatility, with Wall Street maintaining a ‘Moderate Buy’ consensus on the healthcare giant.

According to data from TipRanks, 23 analysts have issued ratings on UnitedHealth over the past three months, including 18 buy ratings, four holds, and one sell recommendation. The average 12-month price target stands at $390.05, implying a potential upside of about 20%.

The highest analyst target on the stock is $444, while the lowest forecast projects shares could fall to $287.

Although analysts remain divided over near-term headwinds facing the healthcare sector, most continue to view UnitedHealth as fundamentally strong due to its dominant insurance and healthcare services businesses.

Specific analyst outlook on UNH stock price

Analysts at Mizuho on May 20 raised their price target on UnitedHealth shares to $440 from $410 while maintaining an ‘Outperform’ rating following what the firm described as solid first-quarter results across the managed care sector. Mizuho said the higher target reflects a reduced likelihood of unfavorable medical loss ratio shifts through the end of 2026, a trend that could support stronger profitability in the coming quarters.

Meanwhile, Goldman Sachs raised its UNH price target to $435 from $400 following the company’s stronger-than-expected first-quarter 2026 results and higher full-year guidance. The bank said the updated outlook reinforces UnitedHealth’s long-term earnings growth potential, with analysts projecting the company can return to annual EPS growth of 13% to 16% over the coming years as its recovery progresses. However, Goldman also highlighted ongoing risks tied to Medicaid funding cuts introduced through recent legislation, which are expected to pressure margins in UnitedHealth’s Medicaid segment through 2026.

At the same time, BofA Securities raised its price target to $371 from $337 while maintaining a ‘Neutral’ rating after the healthcare giant posted stronger-than-expected first-quarter results. BofA noted that UnitedHealthcare margins improved year over year, while Optum margins declined, with some uncertainty around the comparability of Optum subsegment margins. The new target is based on 19 times projected 2027 earnings, up from the prior multiple of 17.3 times.